Onde foi parar a Nova Rota da Seda?

A Iniciativa da Nova Rota da Seda (ou Belt and Road Initiative, BRI), lançada por Xi Jinping, completou seu décimo aniversário este ano. Está neste momento em uma terceira fase.

A Iniciativa da Nova Rota da Seda (ou Belt and Road Initiative, BRI), lançada por Xi Jinping, completou seu décimo aniversário este ano. Está neste momento em uma terceira fase.

The global economic environment has changed as the U.S.—and to a less confrontational degree, the European Union—have clearly established a context of technological rivalry with China. Hindering China’s progress in the sophistication of semiconductor production has become a centerpiece of current U.S. foreign policy. While the U.S. is clearly winning the semiconductor war, the picture is different when it comes to clean-energy technology. Both technology wars overlap with access to and refinement of critical raw materials (CRM), which are key upstream components of the corresponding value chains, encompassing mineral-rich emerging markets and developing economies. The way in which the U.S. and the European Union approach the goal of self-sufficiency, as well as access to and refinement of CRMs, will make a big difference to their stakes in the technology wars.

The surprising victory of Javier Milei, the unconventional ‘anarcho-capitalist’ candidate, in the August primaries ahead of Argentina’s October 2023 general election, can be largely credited to his commitment to dollarize the Argentine economy, a move perceived as the ultimate solution to bring an end to the nation's economic turmoil. The potential shift from the local currency to the dollar has sparked concerns about Argentina's bilateral currency swap line with China. This swap line plays a crucial role in their bilateral relations and has also served as a means for Argentina to fulfill its debt obligations to the International Monetary Fund. The swap line is seen as a key element in preventing Argentina from defaulting on its IMF obligations, which is vital for both its economic and international financial stability. Given the significance of these developments, this article explores Argentina's potential shift towards dollarization and its implications for the country's relationship with China. It does so by assessing the critical role of the bilateral currency swap line between the Central Bank of Argentina (BCRA) and the People's Bank of China (PBOC) in backing Argentina's external payments. The analysis traces the history of the BCRA-PBOC swap line, highlighting how Argentina has relied increasingly on it during financial crises. It also examines the potential challenges and uncertainties that may arise if Argentina does indeed move towards dollarization, including the fate of the swap line and how it would be managed. Additionally, the article reflects on China's strategic approach to swap agreements with partner countries, emphasizing its flexibility in sustaining stable trade relations, even in the face of undesirable political shifts. Finally, it underscores the magnitude of China-Argentina trade relations, particularly in terms of Argentina's significance in helping China secure strategic resources, and how these relations impact Argentina's economic recovery. In conclusion, the fate of the BCRA-PBOC swap line is deeply intertwined with the broader economic and political dynamics between China and Argentina. Both nations are likely to seek pragmatic solutions to address the challenges posed by Argentina's potential shift towards dollarization, thereby ensuring the continuation of stable bilateral relations.

As posições de China e EUA nas tecnologias de energia limpa estão hoje inversas às de semicondutores. A transição para a energia limpa está exigindo tanto a inovação científica quanto a expansão em grande escala de tecnologias estabelecidas. Os EUA permanecem excelentes na primeira, incluindo-se aí o trabalho científico na captura e no armazenamento de carbono e na sua remoção. Por outro lado, nas indústrias comerciais que estão na fase de expansão, os EUA estão atrás da China nas tecnologias de descarbonização mais críticas: solar, eólica, baterias e hidrogênio..

Pares de países têm acordado liquidar transações comerciais e financeiras entre si em suas moedas locais, em geral mediante acordos bilaterais entre seus bancos centrais. A China tem sido capaz de usar sua moeda para liquidar metade de suas transações externas de comércio e investimento. O uso crescente de moedas locais em pagamentos externos será parte do que já chamamos aqui de “desdolarização devagar e limitada”. A “fragmentação” parcial do sistema global de pagamentos está em curso.

Dificultar a progressão da China na sofisticação da produção de semicondutores tornou-se peça central da política dos EUA

The post-‘COVID zero’ reopening of the Chinese economy has improved its growth outlook: the IMF projects 5.2% growth (2023), with declines afterward up to 3.5% in 2028. Will economic reopening and Chinese growth be strong enough to repeat previous contributions to Latin America via exports of food, minerals, and oil? This time it will be more gradual and in a different direction. Financial and investment flows will also be different.

A reabertura pós-COVID zero da economia chinesa melhorou suas perspectivas de crescimento: o FMI projeta crescimento de 5,2% (2023), com quedas posteriores de até 3,5% em 2028. A reabertura econômica e o crescimento chinês serão fortes o suficiente para repetir as contribuições anteriores à América Latina por meio das exportações de alimentos, minerais e petróleo? Desta vez, será mais gradual e em uma direção diferente. Os fluxos financeiros e de investimentos também serão diferentes.

This chapter examines the impacts and durable consequences of Europe’s war (in Ukraine), overlapping with the effects of other components of the ‘perfect storm’ (pandemic, severe weather phenomenon, hunger, global inflation) for Latin America. First, we deal with the global tectonic shifts that have conditioned the region’s economic performance since the 1990s. Second, we outline the range of effects stemming from the ‘perfect storm’. The third section discusses how economic relations between China and Latin America have evolved. Finally, we frame the U.S.-China rivalry in a Latin American context.

Interview with Otaviano Canuto, Senior Fellow at the Policy Center for the New South December 14, 2022

Semicondutores estão no centro da atual rivalidade entre Estados Unidos e China. Dificultar a progressão da China na sofisticação da produção de semicondutores tornou-se peça central da política dos EUA em relação ao país. O caso dos semicondutores se encaixa como uma luva no que observamos nessa coluna como reversão da globalização nos segmentos de alta tecnologia considerados sensíveis desde um ponto de vista de segurança nacional. Com custos, ainda que considerados justificáveis por autoridades governamentais.

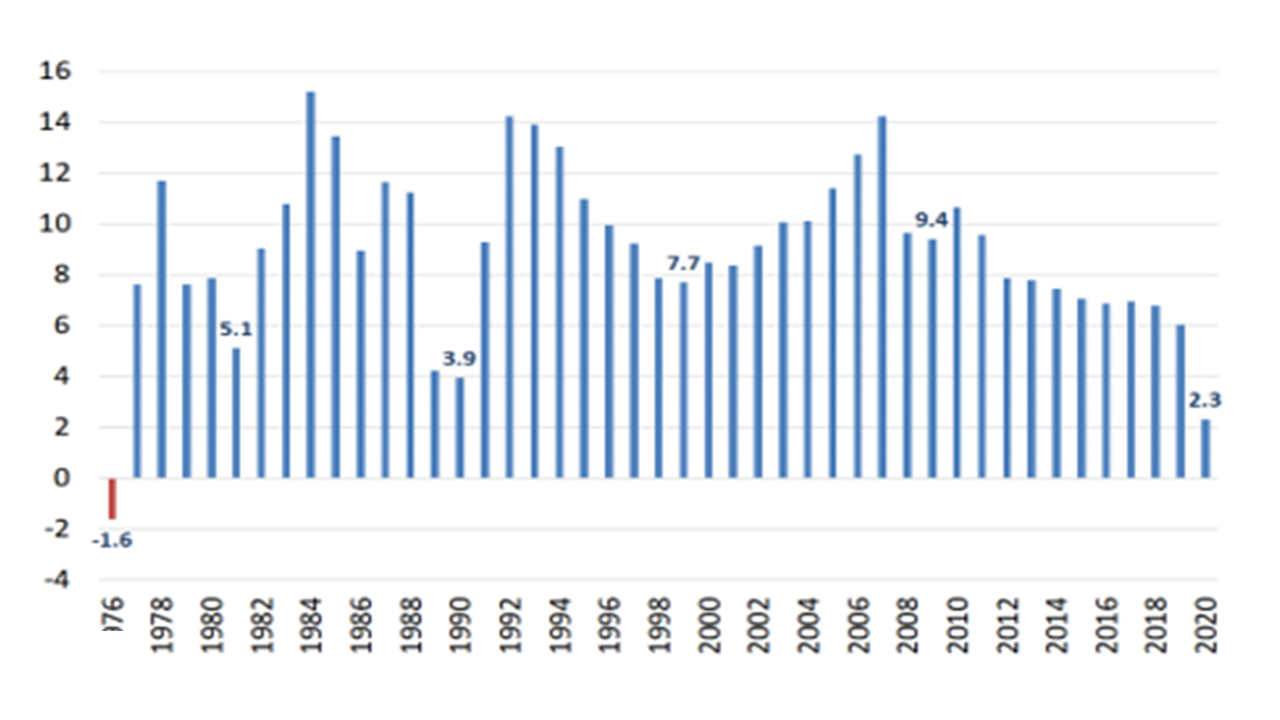

Chinese economic figures released since August’s beginning have shown a slowdown in its growth. New Omicron coronavirus outbreaks in the context of the Covid-zero policy, the housing slump and heat waves have been decelerating the economy’s pace. China’s current growth slowdown is an additional step in the trajectory of gradually declining rates that has accompanied the “great rebalancing” since the beginning of the 2010s. One major difference now is the perception of exhaustion of waves of overinvestment in real estate and infrastructure as a lever, as compared to three previous moments since the beginning of the last decade.

Números da economia chinesa divulgados desde o início do mês mostram uma desaceleração em seu crescimento. Novos surtos de Covid-19 no contexto da política de Covid zero, a queda do setor imobiliário e ondas de calor vêm segurando o ritmo da recuperação econômica do país. Há uma percepção de esgotamento da alavanca de superinvestimentos imobiliários e na infraestrutura. As autoridades chinesas estão optando por salvaguardar sua economia das vulnerabilidades financeiras, mesmo que ao preço de um crescimento do PIB abaixo das metas oficiais.

The heavy financial sanctions on Russia after the invasion of Ukraine sparked speculations that the weaponization of access to reserves in dollars, euros, pounds, and yen would spark a division in the international monetary order. There has been a reduction in the degree of "dollar dominance” with the dollar's share of central bank reserves falling since the beginning of the century. The relative dominance of the dollar appears to be declining but at a very gradual pace.

As pesadas sanções financeiras sobre a Rússia depois da invasão da Ucrânia suscitaram especulações de que o uso armado do acesso a reservas em dólares, euros, libras e ienes iria suscitar uma divisão na ordem monetária internacional. A dominância relativa do dólar parece declinante, mas em ritmo muito gradual.