In: Hormuz and the Invisible Fractures: the Price of a Distant War – Views from the New South

Abdelhak Bassou, Ferid Belhaj, Ian O. Lesser, Marcus Vinicius de Freitas, Rida Lyammouri, Otaviano Canuto, Hafez Ghanem, Hinh T. Dinh, Hugo A. Mansilla

Otaviano Canuto and Hugo A. Mansilla

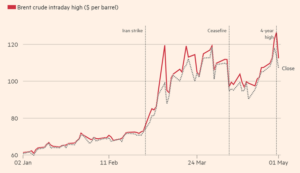

After the joint U.S.–Israeli military action against Iran on February 28, 2026, the closure of the Strait of Hormuz abruptly removed a substantial share of the world’s daily oil supply from accessible markets. The Brent Crude Oil price surged from levels below US$ 80 per barrel to above US$ 126 per barrel by May 1 (Figure 1).

Figure 1: Brent Crude Oil prices January to May 2026.

Source: Ratcliffe, V. and Moore, M. (2026).

It is a price shock comparable in scale to the 1973 oil embargo, though the transmission mechanisms differ markedly in today’s globalized, financialized commodity system (Corbett, 2013). The Strait of Hormuz, through which approximately 30% of global oil trade flows, represents a critical chokepoint (EIA, 2025), making its closure a first-order supply shock with few modern precedents. Fatih Birol—head of the International Energy Agency (IEA)—stated that this war with Iran poses the “greatest threat to global energy ‘in history’”. The most immediate and significant impact of the Middle East conflict is on global energy markets, but it is not the only impact (Canuto, 2026a).

Dual-Edged Effect of the Hormuz Shock on South America’s Mineral Economy

For South America’s mineral economies, the crisis has created a dual-edged shock: higher global prices for key exports such as copper, lithium, iron ore, and oil, coinciding with sharply elevated costs for imported energy, fertilizers, industrial chemicals, and equipment. The net effect is country-specific and sector-specific, producing distinct winners and losers both across and within nations. Understanding that duality requires moving beyond headline prices to examine the structural mechanics beneath them.

The recent price levels reflect more than physical scarcity. A significant portion of the move is attributable to risk-premium inflation in futures markets and speculative amplification that magnifies short-term volatility beyond fundamental supply-demand shifts. In practice, countervailing forces such as IEA strategic petroleum-reserve releases, demand destruction in price-sensitive emerging economies, and emergency rerouting around the Cape of Good Hope would dampen but not negate the shock. A sustained oil price at this level for 90 or more days would, based on historical demand elasticity, reduce global GDP growth by approximately half to one-and-a-quarter percentage points, generating a secondary demand-destruction risk that erodes commodity prices even as supply disruptions persist (IMF, 2026). This “stagflationary” feedback loop is the most underweighted scenario in current assessments of the crisis, and it bears directly on the region’s apparent windfall.

One of the most consequential dimensions of the Strait of Hormuz closure is its effect on fertilizer supply chains (Canuto, 2026a). Approximately one-third of fertilizer raw materials transit the Strait, but that aggregate figure requires careful disaggregation to be actionable (Morningstar DBRS, 2026). The exposure is heavily concentrated in nitrogen-based inputs urea and ammonia, produced in Qatar and Saudi Arabia, while potash, sourced primarily from Canada, Russia, and Belarus, is largely unaffected. Phosphate exposure is moderate, given Saudi Arabia’s Ma’aden complex, with Morocco, China, and the United States providing feasible alternatives.

For South America, the practical consequence fall heavily on Brazil, the world’s largest fertilizer importer, sourcing roughly 85% of its needs from abroad (Mano, 2022) (Canuto, 2026b). The disruption falls disproportionately on nitrogen-based fertilizers used in grain and soy cultivation. Mining operations face separate but related vulnerabilities: sulfuric acid used in copper heap leaching, diesel fuel for heavy equipment, and imported processing machinery are all subject to price escalation under current conditions. Energy already constitutes between 20% and 35% of total copper-mining costs, and that share rises sharply at current oil prices, compressing margins even as copper prices climb.

Brazil’s position within this crisis is the most dual-faced in the region. As a major oil producer with pre-salt field output exceeding four million barrels per day (Petrobras, 2025), Brazil benefits substantially from higher global energy prices, capturing new Asian buyers who are re-routing away from the disrupted Gulf supply. Simultaneously, as the world’s major fertilizer importer, Brazil faces sharply higher input costs for the agricultural and mining sectors that form the backbone of its non-oil export economy. Higher oil export revenues do not automatically offset losses in agricultural productivity driven by fertilizer shortages. The risk is concrete: if nitrogen-based fertilizer disruptions suppress the 2026 soy and corn harvests, Brazil could see export volumes fall precisely when global food prices are rising, creating a damaging feedback loop within its own agricultural trade balance.

Chile’s situation is cleaner on the surface but carries its own internal tension. Elevated copper prices boost export revenues for Codelco and private operators like Antofagasta, and the global energy transition provides a structural long-run demand argument for Chilean copper but the margin of compression from higher energy costs is real and substantial. With Codelco facing operations with thinner margins, the net benefit of higher copper prices may be considerably narrower than headline figures suggest (Hidayat, 2026). A further risk not yet priced in most analyses is that the demand for copper strongly reflects global manufacturing activity. If the oil shock triggers an industrial slowdown, as comparable historical shocks have done, copper demand could fall simultaneously, with continued supply-side cost pressure, eliminating the price windfall entirely and leaving Chile with elevated costs and reduced revenues.

In contrast, Peru and Argentina occupy a cautiously positive position, benefiting from higher global prices for copper, silver, and lithium respectively. The lithium opportunity, however, demands important qualifications. Lithium demand is driven by the structural long-run trajectory of electric vehicle adoption, not by short-run commodity cycles. An oil shock of this magnitude may suppress EV manufacturing output in China and Europe through industrial slowdown, reducing immediate lithium offtake even as it reinforces the multidecade case for the energy transition. The windfall is real but deferred. Political and institutional risk compounds the uncertainty in both countries, given Peru’s persistent mining-sector social conflicts and Argentina’s history of macroeconomic instability.

Guyana and Colombia occupy the most straightforwardly positive position among the region’s oil producers. Both nations are capturing new Asian market share as Atlantic Basin production becomes the preferred alternative to disrupted Gulf supply, and oil revenues are flowing into public budgets that have been preparing for this moment of expanded production capacity (OilNOW, 2025; ExxonMobil, 2025). Supply-chain bottlenecks and infrastructure constraints limit the speed at which gains can be fully realized, but the direction is clearly favorable.

Venezuela’s theoretical windfall is the most constrained of all. Production capacity has fallen to an estimated 700,000 to 900,000 barrels per day, reflecting years of underinvestment, skilled labor emigration, and infrastructure deterioration. Even with oil at three-digit levels of prices per barrel, and the recent easing of U.S. sanctions on Venezuela’s energy sector, there is a windfall in price that cannot be converted entirely into revenue, reinvestment, or public services. This creates a fiscal paradox with considerable humanitarian and political consequences, but its resolution lies outside the scope of commodity markets.

Central American and Caribbean nations represent the cleanest and most troubling case in the region: pure terms-of-trade deterioration with no compensating upside. Except for Trinidad and Tobago, these countries are paying more for energy and imported goods while their export revenues—largely agricultural commodities, tourism receipts, and remittances—do not respond positively to an oil shock. Dollarized or fixed-exchange-rate economies cannot use currency depreciation as a buffer, raising the risk of stress at balance-of-payments, consumer inflation, and fiscal pressure on subsidized energy programs. The uneven distribution of burdens across the region is, in this respect, as important as the windfalls elsewhere.

Most assessments of the crisis correctly identify the dual nature of the shock—higher revenues combined with higher costs—but undervalue several transmission mechanisms that will determine whether the net effect is ultimately positive or negative for the region’s mineral economies. The possibility of a recession feedback loop is a frequent significant omission. Historical precedent from 1973–1974, 1979–1980, and 2008 (Hamilton, 2011) shows consistently that severe oil price spikes precipitate demand contractions that depress nonenergy commodity prices, including the copper, lithium, and iron ore at the center of South America’s export mix. The stagflation scenario with elevated input costs coinciding with falling export prices is not merely possible, but historically the norm, following shocks of this magnitude.

Exchange rate dynamics compound this risk in ways that vary by country. Higher commodity export prices typically strengthen local currencies through the Dutch Disease mechanism, which can undermine export competitiveness in non-resource sectors and create domestic inflation pressures even as external revenues rise (Brahmbhatt et al, 2010). Conversely, if global risk-off sentiment dominates market psychology, currencies may weaken despite higher commodity prices, amplifying domestic inflation without delivering the offsetting export gains. For Argentina in particular, where monetary credibility remains fragile, this channel warrants close attention.

Long-Term Effects of the Hormuz Shock on South America’s Mineral Economy

No shock with the magnitude and extensive scope of the one caused by the Strait of Hormuz crisis ends without leaving a legacy of trajectory changes. Among these, even if coal may be used as a substitute for oil and gas in Asia, the “road to decarbonization” and rising use of critical minerals and rare earth in the world will be reinforced (Canuto, 2021a; IEA, 2021).

This oil supply disruption, the largest in history, has forced a global energy pivot, with higher, permanent risk premiums in energy markets. The conflict has forced countries, particularly in Asia, to accelerate energy diversification away from Middle Eastern oil, and toward more secure, long-term supply sources. A lasting “energy-risk premium” is anticipated, with the potential for structurally higher oil and natural gas prices. Governments are likely to adopt policies favoring larger, long-term strategic reserves of oil and natural gas to reduce reliance on the vulnerable spot market. Furthermore, volatility and high diesel prices for industrial use are strengthening the long-term trend toward electrification in sectors like mining to reduce reliance on oil.

In turn, chronic shortages of critical minerals due to the closure of the Strait of Hormuz will lead to long-term shifts in raw material sourcing. The obstruction of key shipping lanes has forced a global re-evaluation of supply chains for critical minerals, including rare-earth elements. The conflict has hindered plans to expand critical-mineral processing, affecting projects like those in Saudi Arabia aimed at processing African materials. The disruption has caused long-term issues in sourcing raw materials for semiconductors, solar panels, aluminum, and graphite. Additionally, the disruption of refined critical minerals and byproducts like helium and sulfur directly impacts the production of advanced military and technological assets.

South America’s mineral richness—like Africa’s (Canuto & Emran, 2025)—will come to the fore. Chile and Peru together have been the source of approximately 40% of global copper output, and they comprise 35% of known world reserves. Argentina, Bolivia, and Chile constitute “the lithium triangle”, with close to 50% of global lithium resources. Latin America has around 16% of global nickel reserves and 23% of rare earth reserves. Brazil has the world’s second-largest rare-earth reserves and is currently the origin of approximately 90% of global niobium production (Pereira et al, 2026).

Ayres and Juvenal (2026) offer a map of critical minerals in Latin America and the Caribbean (see Table 1). They have also made an illustrative valuation exercise by multiplying the size of known reserves by current international prices to gauge the scale of critical mineral assets in the region. For example:

- Chile’s copper reserves would be valued at more than 500% of GDP, and above 300% of GDP in Peru.

- The estimated value of Brazilian rare-earth reserves would correspond to almost twice the country’s GDP.

- In the “lithium triangle”, Chile’s reserves would be worth 210% of GDP, and Argentina’s 50% of GDP.

- Brazil’s rare-earth reserves are valued at about twice GDP.

- Guatemala and Colombia are also potentially rich in terms of nickel.

These are impressive figures, even reckoning that they are still far below the oil-reserve valuations in Guyana and Suriname, which amount to 35 and 42 times their respective GDPs.

The authors remark that these figures are purely illustrative, as they assume all reserves could be extracted and sold immediately, whereas in reality, extraction requires decades of technical effort, investment, and complex regulatory approvals. And indeed, South America’s mineral landscape exhibits a large gap between endowment and production (Pereira et al, 2026). The point to be taken is the… potential!

Natural wealth may become either a blessing or a curse, as we know (Canuto & Daoulas, 2019) (Canuto, 2021b). Reliable institutions and quality of governance, enabling infrastructure, and appropriate destination of revenues will make the difference in terms of capturing benefits. The boom-bust cycles that have characterized the region’s commodity history for over a century must be avoided.

The most offered policy prescriptions are to invest in domestic input capacity, to diversify trade partners, to enhance regional cooperation, and to identify appropriate strategic directions while remaining insufficiently specific about mechanisms (Tran & Canuto, 2025). The more targeted and economically proven instruments deserve greater attention. Chile’s copper stabilization fund, which accumulates windfall revenues during price peaks to buffer downturns, remains the clearest regional model for managing commodity-cycle exposure (Global SWF, 2024); countries without analogous mechanisms are most vulnerable to the boom-bust dynamic that the current shock is accelerating. Mexico’s long-running oil-price-hedging program provides a direct precedent for locking in current elevated prices against the eventual normalization of the market: an option particularly relevant for Guyana and Colombia at this time of expanded production.

Brazil’s fertilizer vulnerability is the most acute and most tractable supply-chain exposure in the region. Emergency supply agreements with non-Gulf nitrogen producers (Russia, Egypt, Trinidad and Tobago), combined with the development of strategic reserves for the most critical inputs would materially reduce dependence on the disrupted transit corridor. For mining operations across the Andes and Brazil that rely on imported fossil fuels for processing power, investment in regional electricity interconnection and renewable energy for industrial use would reduce the sector’s long-term-cost exposure in a way that no amount of hedging can replicate.

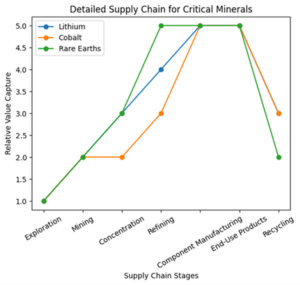

It must also be stressed that accruing benefits from natural wealth includes moving up the value chain toward value addition beyond extraction (Figure 2 illustrates this for lithium, cobalt, and rare earth elements). In addition to upstream activities (such as exploitation, mining, and concentration), midstream (refining) and downstream processes (including battery cathodes, permanent magnets, and end-use products) are equally important in maximizing value capture.

Figure 2: Supply chain for critical minerals.

Source: ChatGPT.

The Strait of Hormuz crisis simultaneously validates South America’s global importance as an alternative commodity supplier and exposes the structural fragility of its input dependency chains. The central tension between windfall revenues and rising operational costs will resolve differently across the region depending on institutional capacity, commodity mix, and whether global growth holds or contracts. Countries with functioning stabilization mechanisms, diversified supply chains, and credible macroeconomic frameworks are best positioned to capture the upside; those without will find the apparent windfall consumed by cost inflation and political dysfunction, and miss an opportunity to build structural resilience.

The lesson of past commodity booms is consistent across cycles and continents: the crisis moment itself is rarely decisive. What follows—whether windfalls are converted into durable infrastructure, institutional capacity, and economic diversification, or consumed in the short-term pressures of the moment—determines long-term outcomes. South America’s resource economies have been offered a narrow window by the upheaval in the Middle East. The actions taken in the months that follow will determine whether the region uses it.

To conclude, it is worth stressing that economies in the region have the chance to explore the opportunities for collaboration opened by both sides of the geopolitical dispute between the U.S. and China (Canuto, 2026c; 2026d).

Table 1: Critical Minerals in Latin America and the Caribbean

| Mineral | Latin American production leaders and potential producers

|

Main uses |

| Aluminum (including bauxite) | Brazil, Guyana, Jamaica, Suriname, Venezuela | Almost all sectors of the economy |

| Antimony | Bolivia, Mexico | Lead-acid batteries and flame retardants |

| Arsenic | Peru | Semiconductors |

| Barite | Mexico | Oil and gas drilling and medical imaging |

| Beryllium | Brazil (potential) | Manufacture of metal alloys for aerospace and defense |

| Bismuth | Bolivia (potential), Mexico (potential) | Nontoxic metals, atomic research, and some medical applications |

| Boron (including borates) | Argentina, Bolivia, Chile, Peru | Hardening of steel and glass and in nuclear energy |

| Rare earths (excluding scandium) | Brazil (potential) | Batteries, permanent magnets, lasers, catalysts, metallurgy, nuclear reactor components, fiber optics, data storage devices, medical imaging, electronics, and some cancer therapies, aerospace metal alloys, ceramics, and colorants |

| Cesium | Chile (potential) | Atomic clocks for global positioning systems |

| Chromium | Brazil | Stainless steel |

| Cobalt | Brazil (potential) | Batteries and metal alloys used in extreme temperatures |

| Copper | Argentina, Chile, Mexico, Panama (potential), Peru | Wiring and cables |

| Fluorspar | Mexico | Synthetic materials and plastics, iron and steel, ceramics, glass, and refineries |

| Graphite | Brazil, Mexico | Lubricants, batteries, and fuel cells |

| Indium | Peru (potential) | Flat-panel displays and touchscreens |

| Lead | Bolivia, Mexico, Peru | Batteries, ammunition, and glass and ceramics production |

| Lithium | Argentina, Bolivia (potential), Brazil (potential), Chile, Mexico (potential), Peru (potential) | Rechargeable batteries |

| Magnesium | Brazil | Metal alloys used by aerospace, automotive, and electronics industries |

| Manganese | Brazil, Mexico | Steel production and batteries |

| Nickel | Brazil, Colombia, Dominican Republic, Guatemala | High-strength steel and rechargeable batteries |

| Niobium | Brazil | Strengthening of steel |

| Phosphate | Brazil, Mexico, Peru | Fertilizers |

| Potash | Brazil, Chile | Fertilizers |

| Rhenium | Chile, Peru | High-performance jet engines and gas turbines |

| Rubidium | Peru (potential) | Atomic clocks for global positioning systems, data network syncing, and research and development |

| Silicon | Brazil, Venezuela (potential) | Silicon wafers fundamental to semiconductors |

| Silver | Argentina, Bolivia, Chile, Mexico, Peru | Electrical circuits, batteries, solar cells, and antibacterial medical instruments |

| Tantalum | Bolivia (potential), Brazil | Materials and electronic components that need to withstand high temperatures and harsh environments |

| Tin | Bolivia, Brazil, Peru | Food and beverage cans, circuit board components, and corrosion-resistant metal coatings |

| Titanium | Mexico (potential, mainly through the titanium dioxide pigment sector) | White pigment and in metal alloys, including for airplanes, spacecraft, and military vehicle armor |

| Tungsten | Bolivia | Wear-resistant metals for jet engines, ammunition, and mining and cutting equipment |

| Uranium | Brazil (potential) | Nuclear fuel and medical applications |

| Vanadium | Brazil | Strengthening of iron and steel |

| Zinc | Bolivia, Mexico, Peru | Coating to protect iron and steel from rust and corrosion |

Source: Ayres & Juvenal (2026).

References

Atlantic Council Experts (2026). “How the Iran War Could Shift Energy Policies Around the World”, April 3.

Ayres, J., & Juvenal, L. (2026). “2026 Latin American and Caribbean Macroeconomic Report: Resilience and Growth Prospects in a Shifting Global Economy”. IDB—Inter-American Development Bank, March.

Brahmbhatt, M.; Canuto, O.; and Vostroknutova, E. (2010). “Dealing with Dutch Disease”, World Bank, Economic Premise n. 16, June.

Canuto, O. & Daoulas, C. (2019). “Natural Wealth and Economic Growth: The Case of Sub-Saharan Africa”, Policy Center for the New South, Policy Paper PP-19/12, August.

Canuto, O. (2021a). “Decarbonization and ‘Greenflation’”, Policy Center for the New South, PB-51/21, December.

Canuto, O. (2021b). “Climbing a High Ladder—Development in the Global Economy”, Policy Center for the New South, February 26.

Canuto, O. & Emran, S. (2025). “Africa’s Minerals Will Shape the Future of Global Power”, Project Syndicate, May 2.

Canuto, O. (2026a). “Dire Strait of Hormuz: A Chokepoint for Global Food and Energy”, Policy Center for the New South, May.

Canuto, O. (2026b). “Transmission Channels of the War on Iran to the Brazilian Economy”, Policy Center for the New South, April 1.

Canuto, O. (2026c). “The New South as a Frontline of the U.S.-China Technological Rivalry”, Policy Center for the New South, PB-07/26, February 11.

Canuto, O. (2026d). “U.S., China, and Latin America: How Far Does the Donroe Doctrine Go?”, Policy Center for the New South, April 30.

Corbett, M.(2013). “The 1973 Oil Crisis”, Federal Reserve History, November 23.

EIA—U.S. Energy Information Administration (2025). “The Strait of Hormuz is the World’s Most Important Oil Chokepoint”, June 16.

ExxonMobil (2025). “Guyana Project Updates: Uaru and Yellowtail Development”, ExxonMobil Investor Relations.

Global SWF (2024). “Chile Economic and Social Stabilization Fund (ESSF) Profile”, Global SWF.

Hamilton, James D. (2011). “Historical Oil Shocks”, National Bureau of Economic Research, February.

Hidayat, M. (2026). “Chilean Copper Production Falls as Codelco Faces Operational Challenges”, Discovery Alert, April 11.

IMF—International Monetary Fund (2026). “World Economic Outlook”, April.

IEA—International Energy Agency (2021). “The Role of Critical Minerals in Clean Energy Transitions”, May.

Mano, A. (2022). “Brazil Reliance on Imported Fertilizer Rises to 85%”, Reuters, January 17.

Morningstar DBRS (2026).“Iran Conflict Could Have Far-Reaching Consequences for Fertilizer Supply Chains”, April 22.

OilNOW (2025). “Guyana Oil & Gas: What to Look Forward to in 2026”, December 31.

Pereira, D.W.; Goldin, J; Barbeito, L.; & Moreira, V. (2026). “South America: The critical minerals frontier”, in J.P. Morgan, Global Data Watch, April 2.

Petrobras (2025). “Pre-salt: Dive into this Ultra-Deep Journey”, October.

Ratcliffe, V. and Moore, M. (2026). “Oil Market One Month from Crunch Point as Global Stockpiles Dwindle”, Financial Times, May 1.

Tran, H. and Canuto, O. (2025). “Asian Economic Integration Led by Trade Liberalization: A Lesson for Other Regions”, Policy Center for the New South, PB – 36/25, July.

Otaviano Canuto is a Senior Fellow at the Policy Center for the New South, Affiliate Professor at Mohammed VI Polytechnic University and Non-Resident Senior Fellow at Brookings Institute. Former Vice President and Executive Director at the World Bank, Executive Director at the International Monetary Fund (IMF), Vice President at the Inter-American Development Bank, and Deputy Minister of Finance for International Affairs of Brazil.

Hugo A. Mansilla is Principal of Avanço Consulting, an advisory firm specializing in geopolitical and economic consultation for both public and private sector clients across multiple areas of governance. Before transitioning to the private sector, Mr. Mansilla served as an analyst within the Climate Change department of the World Bank Group, where he contributed to the Economics of Adaptation to Climate Change (EACC) study.

This Post Has One Comment

Pingback: O Choque de Ormuz, Descarbonização e os Minerais da América do Sul – Center for Macroeconomics and Development

Comments are closed.