In: Hormuz and the Invisible Fractures: the Price of a Distant War – Views from the New South

Abdelhak Bassou, Ferid Belhaj, Ian O. Lesser, Marcus Vinicius de Freitas, Rida Lyammouri, Otaviano Canuto, Hafez Ghanem, Hinh T. Dinh, Hugo A. Mansilla

The U.S. airstrike in February that killed top leaders of the Iranian regime initiated a war involving the United States and Israel against the country of Iran. After more than a month of mutual bombardments between Iran and Israel ensued, the conflict extended to other Persian Gulf nations and U.S. military installations. From a global perspective, the impact of this conflict has stemmed primarily from disruptions to the regional production of goods and the blockade of the Strait of Hormuz.

Iran’s disruption of transportation via the Strait of Hormuz—the most vital passageway for the world’s energy supply—has been a weapon utilized since the start of the conflict, and has also been accompanied by a blockade by the U.S. Navy. Cross attacks stopped—or almost—with a two-week ceasefire announced on April 8, but traffic through the Strait of Hormuz remained restricted.

The outbreak of conflict in the Middle East has triggered a multilayered shock to the global economy and financial markets. The severity of global consequences will depend on the duration of disruptions—particularly to the Strait of Hormuz—and the policy responses of governments and central banks.

We address here the transmission channels through which the conflict has affected global energy markets, commodity supply and prices, transportation systems, macroeconomic conditions, and financial markets. Rather than focusing only on oil and gas supply, we trace how the disruption in the Strait of Hormuz and to related infrastructure has potentially propagated through shipping, aviation, food costs, remittances, inflation expectations, and central bank responses. Although short-term disruptions may produce volatility without structural transformation, prolonged conflict risks leading to stagflation, changes to trade patterns, and reshaping of global financial dynamics.

Energy Market Disruptions and Global Supply Shocks

It is no coincidence that Fatih Birol—head of the International Energy Agency (IEA)—stated that a war with Iran poses the “greatest threat to global energy ‘in history’”. The most immediate and significant impact of the Middle East conflict is on global energy markets. The Strait of Hormuz, through which approximately 30% of global oil trade flows, represents a critical chokepoint. Even a temporary disruption has outsized consequences for global supply chains and price charging.

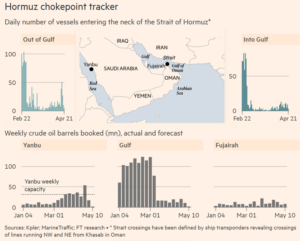

Figure 1 reveals how the traffic of vessels has been affected since the start of the conflict, and the reduction in the numbers of crude oil barrels booked. It is important to remember that until April the oil—and other shipments—that crossed the strait before the war were still reaching their destination, but since the closure of the strait and the blockade, the effects on physical supply constraints are starting to be fully felt. There is a sequence, with current and future price shocks coming first, followed by physical supply constraints afterwards. The Iran shock has already moved beyond a pure price shock, as ships that have crossed the Hormuz before the start of the war have reached their destinations. The ceasefire feeds hope of a gradual normalization, while the possibility of accelerating physical breakdown remains.

Figure 1: Hormuz chokepoint tracker.

Source: Financial Times, April 21, 2026.

The attacks on energy infrastructure in the Gulf and the closure of the Strait of Hormuz disruption have removed 12 million barrels per day from global oil supply, according to Russell Hardy, from Vitol (Wilson and Moore, 2026), leading to inventory drawdowns and pushing Brent crude prices to around US$ 90 per barrel (bbl) (Figure 2). This price increase reflects not only the physical loss of supply but also a geopolitical risk premium embedded in market expectations.

Figure 2: Oil prices

Source: Alpine Macro, U.S. Themes and Strategy, April 16, 2026

Although the conflict remains unresolved and disruptive tail risks still linger, most analysts’ perceptions of the risk have diminished, leading to a baseline scenario which incorporates an opening of the strait sometime in the coming weeks. But in a more serious scenario—with, say, a disruption longer than three months—the consequences become dramatically more pronounced.

According to Natixis (2026), theoretically, oil prices could rise above US$ 170 per barrel, based on supply–demand fundamentals, although strategic reserves and demand destruction would likely cap prices at lower levels, perhaps around US$ 115 per barrel. Brent closed around US$ 105 on April 26, while West Texas Intermediate, the U.S. marker, closed at US$ 94.40. The absence of comparable strategic reserves in natural gas markets makes gas prices even more sensitive, with European gas prices, under prolonged disruption, potentially exceeding € 100/MWh.

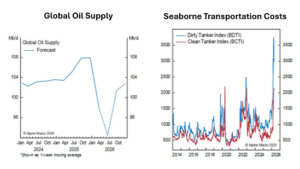

As an optimistic baseline scenario, the Alpine Macro (2026) research team has estimated that the return of crude oil output currently offline will be gradual over the next one to three months. This is consistent with Brent futures prices not far from near-dated futures at US$ 95/bbl and US$ 88/bbl one and three months out, respectively, alongside the explosive rise in seaborne costs of transporting both crude and refined oil products (Figure 3).

Figure 3: Global oil supply and seaborne transportation costs

Source: Alpine Macro, U.S. Themes and Strategy, April 16, 2026.

Alpine Macro (2026) expects oil to settle somewhere around US$ 70–80/bbl in the short term , in the case of an end to hostilities, with a residual geopolitical risk premium of US$ 5–10/bbl compared to prewar levels, that will likely remain over this period, as a result of higher maritime transportation and insurance costs, as well as the time required to repair and fully restore damaged energy infrastructure.

According to the IEA, as of the end of March, more than 40 energy facilities across Gulf producers had sustained severe damage during the conflict. Restoration of output should take weeks to months, depending on the extent of the damage. The two most severely damaged pieces of infrastructure relate to natural gas rather than oil. According to Amrita Sen, from Energy Aspects, in the case that 50% of traffic through the Strait of Hormuz comes back by the end of May, 450mn barrels of clean refined products, such as diesel and gasoline, will have been lost by the market (Wilson and Moore, 2026).

Oil demand is relatively inelastic in the short run, meaning that large price increases are required to reduce consumption. However, over time, sustained high prices can lead to behavioral changes, reduced economic activity, and substitution of alternative energy sources.

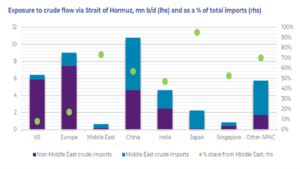

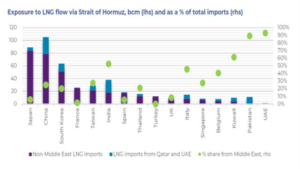

The energy shock also has asymmetric regional effects. Asia is particularly vulnerable due to its heavy reliance on Middle Eastern energy imports (Figures 4a and 4b). Countries such as Japan and India face high exposure, with limited immediate alternatives.

Figure 4a Exposure to crude flow via Strait of Hormuz

Figure 4b: Exposure to LNG flow via Strait of Hormuz

Source: Natixis, Middle East Conflict: Counting the Shocks on the Global Economy and Impact on Financial Markets, March 10, 2026

Europe, while less directly dependent on Middle Eastern oil, remains vulnerable through global price transmission mechanisms and its dependence on liquefied natural gas (LNG). In Latin America and sub-Saharan Africa, commodity exporters may benefit while import-dependent economies are being negatively impacted through external balances, inflation, and fiscal dynamics.

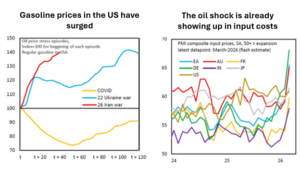

Effects are asymmetric, differentiated according to whether a country is an exporter or importer of oil and gas. Figure 5, taken from Estevão et al. (2026), shows how gasoline prices have surged in the U.S. (left), and how a rise in input costs has been a general feature (right). The transmission is no longer confined to crude benchmarks, with refined products, feedstock, and logistics still carrying the shock into the real economy. In any case, a cliff edge may still be faced if blockades are prolonged.

Figure 5: Gasoline prices and input costs in the US

Source: Estevão, M.; Forton, J.; and Hamilton, L. The Iran Shock: From Prices to Constraints, IIF Global Macro Views, Institute of International Finance, April 16, 2026.

Whether the war ends in a negotiated settlement or in a frozen standoff, it is possible that transit in the Strait of Hormuz will not return to prewar levels. As Kristalina Georgieva, IMF Managing Director, said in a presentation during the IMF–World Bank Spring Meetings: “Even in a best case, there will be no neat and clean return to the status quo ante”.

Commodity Markets Beyond Energy and Global Food Security

The conflict’s impact extends beyond oil and gas into broader commodity markets, particularly metals and industrial inputs. The Middle East plays a significant role in the production of aluminum and sulfur, both of which are critical to global manufacturing and resource extraction.

Aluminum prices have already increased due to disruptions affecting approximately 8% of the global supply. While some of this increase may be temporary, prolonged conflict could sustain elevated prices due to higher energy costs and transportation disruptions.

The war-affected Middle East has become an indispensable engine of modern agriculture and industrial manufacturing (Hanieh, 2026). The disruption to sulfur and sulfuric acid supply chains is a major concern. Sulfuric acid is essential for the extraction of metals such as copper and nickel.

The region provides 45% of globally traded seaborne sulfur. This byproduct of oil and gas desulfurization is the primary feedstock for sulfuric acid, a fundamental input required not just for phosphate fertilizers, but for copper mining, battery metals, and semiconductor fabrication.

The implications for nickel are particularly severe. Indonesia, which produces over half of the world’s nickel, relies heavily on imported sulfur. Supply disruptions could, therefore, constrain production and increase prices, especially for battery-grade nickel used in electric vehicles.

Furthermore, the Gulf provides roughly 30% of internationally traded ammonia—the starting point for all mineral nitrogen fertilizers. Saudi Arabia and Oman are respectively the world’s second and sixth largest exporters of ammonia. State-owned giants like Saudi Aramco and Adnoc (UAE) have moved down the value chain, using financial surpluses to dominate the production of finished fertilizers like Urea, DAP (Diammonium phosphate), and MAP (Monoammonium phosphate) The paralysis of the Strait of Hormuz has created a “double squeeze” on global supply chains, provoking a “cascading industrial and agricultural squeeze”, as remarked by Hanieh (2026). Figure 6 shows how the world’s top importers of fertilizer depend on the Gulf.

Figure 6: Top sulphur, urea and ammonia importers in 2025.

Source: Hanieh, A.; The Coming Global Food Crisis, Financial Times, April 18, 2026.

There is also an important Morocco–Gulf link: Morocco, the world’s largest phosphate producer, is deeply dependent on the Gulf, which provides 75% of its sulfur and 30% of its ammonia. Without these Middle Eastern inputs, Morocco’s ability to supply the world with phosphate fertilizers is crippled.

In March, fertilizer prices rose 26.2%. The UN Food and Agriculture Organization warns that if the crisis persists through the first half of the year, prices could sustain levels 15% to 20% higher than previous averages, coinciding with the Northern Hemisphere’s crucial spring planting (FAO, 2026).

The deeper integration of the Gulf into the global food system means that regional shocks now cascade rapidly from “farm to shelf”. Import-dependent nations are the hardest hit. In 2024, Sudan imported 54% of its fertilizers from the Gulf, followed by Sri Lanka (36%) and Tanzania (31%). These nations lack the fiscal buffers to subsidize farmers against the 2026 price shocks.

The World Food Programme (2026) estimates that the war will push an additional 45 million people into acute hunger, with two-thirds of those affected located in Africa. Sudan, where famine conditions are already appearing amidst the world’s worst displacement crisis, is the direst case.

Because of the war there are also high-tech bottlenecks and semiconductor vulnerability. With seaborne sulfur exports largely paused, mining operations in Chile and Australia face soaring costs for copper and battery metal extraction. Simultaneously, the semiconductor and EV sectors see foundational input costs rise, as nitric and sulfuric acid outputs decline.

Constraints in the global supply of highly purified helium complete this picture of modern supply chain vulnerability (Natixis, 2026). The state of Qatar reliably supplies approximately one-third of the world’s critical helium requirements, extracted as an integrated byproduct of its natural gas liquefaction operations. The broader Gulf disruptions have hampered production schedules, while restricted access to the Strait of Hormuz prevents remaining packaged cargoes from reaching vital Asian semiconductor fabrication plants.

Helium remains fundamentally irreplaceable in advanced semiconductor manufacturing processes. It uniquely cools delicate processing equipment during extreme ultraviolet lithography and purges disruptive oxygen during silicon crystal growth. Top-tier consumer chipmakers consequently face unavoidable production adjustments at a historical moment when enterprise demand for computing hardware is steadily expanding

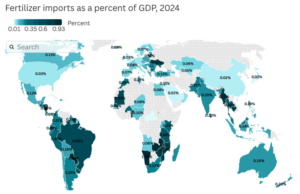

The current conflict is fundamentally different from previous shocks. Because the Gulf states now control the logistical corridors and chemical inputs for global agribusiness, any prolonged disruption to regional infrastructure threatens the structural stability of global food security and the high-tech industrial economy. Regionally, countries in Africa, South America and South and Southeast Asia spend the largest portion of GDP on fertilizer imports (Figure 7).

Figure 7: Fertilizer imports as a percent of GDP

Source: Svenstrup, M.; Martinez, M.; and Landers, C.; Will the Iran War Be the Breaking Point for Vulnerable Countries? Center for Global Development, March 20, 2026.

Transportation and Trade Disruptions

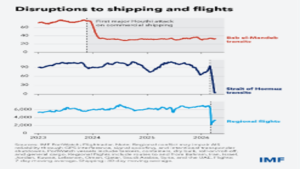

The conflict has also disrupted global transportation networks, affecting both maritime shipping and air travel (Figure 8). The closure of the Strait of Hormuz has reduced oil and LNG shipments, while broader geopolitical instability has impacted shipping routes and insurance costs.

Figure 8: Disruptions to shipping and flights

Source: Georgieva, K.; Cushioning the Middle East War Shock, April 9, 2026.

Some shipping sectors have benefited in the short term. Delays in Suez Canal traffic have helped rebalance supply–demand dynamics in the shipping industry, temporarily boosting freight rates. However, these benefits are likely to be short-lived if demand weakens due to higher costs and economic uncertainty.

Air travel has been more negatively affected. Airport closures and rerouted flights have increased costs for airlines, particularly in Europe and the Middle East. Fuel costs—already a major component of airline expenses—have risen sharply, further compressing margins.

Tourism is another sector at risk. While historical patterns suggest that tourism tends to recover quickly after geopolitical shocks, prolonged instability could damage the region’s reputation as a travel destination, particularly for Gulf economies that rely on tourism for diversification.

Macroeconomic Impacts: Inflation, Growth, and Stagflation Risks

At the macroeconomic level, the conflict introduces a classic supply-side shock: rising input costs combined with slowing growth. This combination raises the risk of stagflation—a scenario characterized by high inflation and weak economic activity.

One may identify several transmission channels through which the ongoing conflict affects global economies:

- Higher energy and food costs: Increased oil and gas prices raise production and transportation costs across industries, leading to higher consumer prices. Higher prices and less availability of fertilizers may also impact food production.

- Trade disruptions: Reduced shipping capacity and higher costs hinder global trade flows.

- Financial tightening: Increased uncertainty leads to tighter financial conditions and reduced investment.

- Income effects: Reduced remittances and tourism revenues affect household incomes in vulnerable economies.

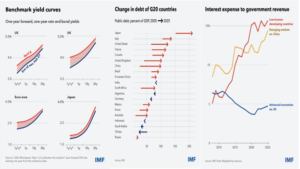

As Georgieva (2026) showed in her presentation during the IMF–World Bank Spring Meetings, markets have been expecting major central banks to tighten their policy stance (Figure 9, left). This is happening in a context in which public debt is generally much higher than 20 years ago—including in most G20 countries (Figure 9, center)—and interest payments are rising as a share of revenue at all income levels (Figure 9, right).

Figure 9: Yield curves, debt of G20 countries, and interest expense to government revenue

Source: Georgieva, K.; Cushioning the Middle East War Shock, April 9, 2026.

It is relevant to call attention to the fact that the current shock is happening at a moment of debt distress for many developing countries (Songwe, 2026). Developing countries paid US$921 billion in interest in 2024. As the war drives up energy and food prices, inflationary pressures are forcing interest rates higher, making finance scarcer for the 3.4 billion people living in countries that spend more on debt service than on health or education.

Svenstrup et al (2026) explore what may make the Iran war “a breaking point for vulnerable countries”. They point out six transmission mechanisms from the Middle East conflict to Emerging Market vulnerability: (1) net energy imports, (2) fossil fuel subsidies, (3) external debt service obligations, (4) fertilizer imports, (5) Gulf-origin remittances, and (6) reserve/import ratio.

A range of potential disruptions to the global economy are detailed in the IMF’s World Economic Outlook report released during the Spring Meetings (IMF, 2026). It sets out three scenarios: (1) the reference forecast scenario, (2) the adverse scenario, and (3) the severe scenario. Considered to be the baseline and most likely scenario, the reference forecast sees global growth falling to 3.1% this year, revised down from 3.3% in January, and headline inflation rising to 4.4%. The adverse scenario—which assumes continued supply chain disruption and higher energy prices—sees growth fall to 2.5% and inflation rises to 5.4%. The least likely but most severe scenario—which assumes supply disruptions continue through next year—sees global growth tumble to 2% and inflation surge above 6%.

Financial Market Reactions and Asset Allocation

Financial markets have responded to the conflict with increased volatility and a shift toward safe-haven assets. The U.S. dollar and Swiss franc have appreciated, reflecting investor demand for stability.

Equity markets have shown divergent performance. U.S. equities have outperformed, reflecting relative economic resilience and safe-haven status. In contrast, Asian and emerging market equities have lagged due to their greater exposure to energy shocks and trade disruptions.

Bond markets have also reacted, widening spreads in European sovereign debt, particularly for countries such as France and Italy. This reflects increased fiscal risks and uncertainty.

In foreign exchange markets, the initial strengthening of the U.S. dollar is expected to reverse over time, particularly if the conflict remains contained. One may also anticipate a recovery in the euro and yen against the dollar in the longer term.

Real estate markets may also be affected. Increased geopolitical risk could drive investment toward perceived safe-haven regions, particularly in Western Europe and parts of Asia.

Policy Responses and Strategic Implications

Government and central bank responses will play a critical role in shaping the ultimate economic impact of the conflict. Key policy tools include:

- Strategic reserve releases: Governments can release oil reserves to stabilize prices and offset supply disruptions. However, the lack of equivalent reserves for natural gas limits policy options in that market.

- Monetary policy adjustments: Central banks may adjust interest rates in response to inflation and growth dynamics.

- Fiscal measures: Subsidies and targeted support can mitigate the impact on households and businesses.

- Trade policies: Export restrictions and protectionist measures may be used to secure domestic supply.

Figure 10 lists national energy policy measures that have already been adopted.

Figure 10: National energy policy responses

Source: Georgieva, K.; Cushioning the Middle East War Shock, April 9, 2026

In the longer term, the conflict may accelerate structural changes in global energy markets. Countries may seek to diversify energy sources, increase domestic production, and invest in renewable energy to reduce dependence on geopolitically sensitive regions.

Differentiated Regional and Country Impacts

The Middle East conflict represents a significant exogenous shock to the global economy, with far-reaching implications across energy markets, commodities, transportation, and financial systems. While short-term disruptions may lead to temporary volatility, prolonged conflict poses a more serious threat, including the risk of stagflation, structural shifts in trade patterns, and sustained financial instability.

The analysis underscores the central role of energy markets in transmitting geopolitical shocks. Disruptions to the Strait of Hormuz have cascading effects across global supply chains, commodity markets, and macroeconomic conditions. At the same time, the impact is unevenly distributed, with Asia and energy-importing economies bearing the greatest burden.

Asia emerges as the most affected region outside the Middle East. Countries such as Thailand, South Korea, and the Philippines face rising import costs, worsening current account balances, and increased inflation.

In China, stockpiles, domestic coal and renewable energy capacity, and price controls have mitigated the shock from the crisis and given China some breathing room for oil and gas. However, a weaker global demand for its exports will bring consequences (Eurasia Group, 2026).

Europe faces a more moderate but still significant impact. While not directly affected by supply disruptions, higher energy prices could slow growth and increase inflation. The extent of the impact depends on the duration of the conflict. A short disruption would have limited effects, while a prolonged conflict could lead to sustained inflation and tighter monetary policy.

In the United States and Canada, the impact is somewhat mitigated by domestic energy production. However, sustained high oil prices could still lead to higher inflation and slower growth. The impact of the Iran war will persist even after the conflict ends, as higher fuel prices feed through into businesses and the wave of inflation remains (McCormick et al, 2026).

Latin America and the Caribbean face a mixed outlook. While oil producers (Argentina, Brazil, Colombia, Ecuador, Guyana, Trinidad and Tobago, and Venezuela) may benefit from higher prices, the region is likely to experience weaker growth, higher inflation, and currency depreciation. As an example, while Brazil’s production and exports of oil will gain in terms-of-trade, rising prices of imported diesel and fertilizers will hurt (Canuto, 2026). Tourism-dependent Caribbean economies, vulnerable-to-energy-prices Central America, and countries with current account deficits that rely on global financing will all suffer (Chalk, 2026).

The economic shock has rippled across Africa. The International Monetary Fund (IMF, 2026) recently revised sub-Saharan Africa’s 2026 growth forecast down to 4.3%, citing the war as a primary driver for reversing the continent’s post-2024 recovery.

The impact is generally split into two camps: a temporary revenue windfall for oil exporters (like Nigeria and Angola) and a severe cost-of-living crisis for oil importers. Higher oil prices increased transport and electricity costs and, given that the Gulf is a major source of global fertilizers—complementary but not perfect substitutes to Moroccan ones—African agricultural productivity is under threat, raising fears of a supply scarcity.

There is also a maritime rerouting at play. As the Red Sea becomes a high-risk zone, shipping is being diverted around the Cape of Good Hope. While this increases traffic for South African ports, it drastically raises freight costs and delivery times for East and North African trade.

African currencies (notably the South African rand and Kenyan shilling) have depreciated, and servicing dollar-denominated debt has become significantly more expensive—something of concern owing to the debt vulnerability of developing countries in the region. According to Selassie (2026):

More than one-third of countries are at high risk of, or already in, debt distress. In 21 countries, fiscal deficits exceed the levels that are needed to stabilize debt. Rising interest bills and dwindling concessional finance are inflating debt-service burdens and crowding out essential development spending.

Additionally, there will be investment delays, since wealthy Gulf nations (such as Saudi Arabia, UAE, and Qatar) are reportedly reevaluating or delaying more than US$ 100 billion in planned African infrastructure investments in order to focus on their own domestic security and repairs.

Morocco finds itself in a particularly delicate position due to its high energy dependence and its strategic alignment with Gulf partners. Unlike its neighbor, Algeria, Morocco is a net energy importer. The surge in oil and gas prices is putting immense pressure on the national budget. The government faces a dilemma: either increase subsidies to protect citizens from inflation (which strains the deficit) or pass costs to the public, risking social unrest.

The war threatens the remittance flows and direct foreign investment (FDI) it traditionally receives from the Gulf Cooperation Council (GCC). Furthermore, as global stability erodes and airspaces face closures or rerouting, Morocco’s vital tourism sector is seeing a cooling effect. Potential travelers are wary of the broader regional instability, even if Morocco remains physically distant from the kinetic conflict.

As global fertilizer supplies from the Gulf are disrupted, Morocco—a world leader in phosphates—may see increased demand and higher prices for its exports, potentially offsetting some of its energy losses, as long as its dependence on sulfur and ammonia from the GCC does not become a barrier to that.

Final Remarks

As the Middle East has assumed a pivotal position in globalization much far beyond just oil and gas production, the unfolding crisis in the region has brought consequences of global reach: a major, multifaceted shock, as well as a possible recalibration of the terms of the geoeconomic competition between China and the U.S. (Zaoui, 2026).

Ultimately, the severity of the economic consequences will depend on the duration of the conflict and the effectiveness of policy responses. Strategic reserves, monetary policy, and international coordination will be critical in mitigating the impact. However, the conflict also highlights the vulnerability of the global economy to geopolitical risks and underscores the importance of diversification and resilience in energy and trade systems.

References

Alpine Macro; “U.S. Themes and Strategy”, April 16, 2026.

Canuto, O.; “Transmission Channels of the War on Iran to the Brazilian Economy”, Policy Center for the New South, April 1, 2026.

Chalk, N.; “The Middle East War Will Have an Uneven Impact on the Western Hemisphere”, IMF Blog, April 17, 2026.

Estevão, M.; Forton, J.; and Hamilton, L.; “The Iran Shock: From Prices to Constraints,” IIF Global Macro Views, Institute of International Finance, April 16, 2026.

Eurasia Group; “China’s Hormuz Resilience Masks Deeper Vulnerabilities”, April 23, 2026.

FAO—Food and Agriculture Organization of the United Nations; “FAO Chief Economist Warns of Severe Global Food Security Risks from Disruption to Strait of Hormuz Trade Corridor”, March 26, 2026.

Georgieva, K.; “Cushioning the Middle East War Shock”; Speech at the 2026 Spring Meetings in Washington, DC

Hanieh, A.; “The Coming Global Food Crisis”, Financial Times, April 18, 2026.

IMF—International Monetary Fund; World Economic Outlook, Ch.1 “Global Prospects and Policies”, April 2026.

McCormick, M.; Stephanie, F.; Meyer, G.; and Roeder, O.; “Impact of Iran War Will Hurt U.S. Even After Conflict Ends, Economists Warn”, Financial Times, April 20, 2026.

Natixis; “Middle East Conflict: Counting the Shocks on the Global Economy and Impact on Financial Markets”, March 10, 2026

Selassie, A.A.; “Africa Faces Mounting Risks Just as Growth Gains Take Hold”, IMF Blog, April 23, 2026.

Songwe, V.; “America’s War Is Adding to Africa’s Debt Burden”, Project Syndicate, April 9, 2026.

Svenstrup, M.; Martinez, M.; and Landers, C.; “Will the Iran War Be the Breaking Point for Vulnerable Countries?”, Center for Global Development, March 20, 2026.

Wilson, T. and Moore, M.; “Oil Market Has Lost a Billion Barrels due to Iran War, Vitol Boss Warns”, Financial Times, April 21, 2026

Zaoui, A.; “Geoeconomic Rebalancing after the Gulf Crisis”, ORF Middle East, April 21, 2026.

This Post Has 33 Comments

The post does a good job highlighting how the Strait of Hormuz is more than an energy chokepoint—it also has major implications for global food supply chains and inflation. What stands out is how a regional conflict can quickly create ripple effects for countries far removed from the Middle East, especially those that depend heavily on imported fuel and agricultural inputs.

The article does a good job highlighting how the Strait of Hormuz is far more than an energy chokepoint—it also has significant implications for global food security and supply chains. One aspect that deserves even more attention is how prolonged disruptions could disproportionately affect import-dependent developing countries, where higher transport and commodity costs can quickly translate into inflation and social pressure.

The article highlightsComment Creation Strategy how disruptions in the Strait of Hormuz can ripple far beyond the Gulf region, affecting both energy markets and global food supply chains. One aspect that deserves more attention is how prolonged shipping uncertainty can raise transportation and fertilizer costs, creating additional pressure on food-importing countries that are already vulnerable to price shocks.

OneBlog Comment Creation Guide point that stood out is how the Strait of Hormuz functions as more than an energy chokepoint—it also has major implications for global food supply chains through higher transportation and input costs. The article does a good job highlighting how regional conflicts can create economic ripple effects far beyond the immediate area, affecting countries that have little direct involvement in the war.

The article highlights how the Strait of Hormuz functions as a critical chokepoint not only for energy markets but also for broader supply chains that affect food prices worldwide. One aspect that deserves more attention is how prolonged disruptions could disproportionately impact import-dependent developing economies, where higher transport and energy costs often translate quickly into inflation and food insecurity.

The article does a good job highlighting how the Strait of Hormuz is not just an energy chokepoint but also a critical link in global food supply chains. One aspect worth emphasizing is that even short-term disruptions can have outsized effects on import-dependent countries through higher shipping costs, insurance premiums, and commodity price volatility. It’s a reminder that regional conflicts can create economic ripple effects far beyond the immediate area.

One of the most important points here is that disruptions in the Strait of Hormuz affect far more than oil markets. The ripple effects on food supply chains, shipping costs, and import-dependent economies can be significant, showing how a regional conflict can quickly become a global economic challenge. It would be interesting to explore how countries can diversify trade routes and build resilience against these chokepoint risks.

The post does a good job highlighting how the Strait of Hormuz is more than an energy chokepoint—it also affects global food supply chains through higher transportation and input costs. One aspect worth exploring further is how prolonged disruptions could impact food-importing developing countries, which are often the most vulnerable to price shocks even when the conflict is geographically distant.

One point that often gets overlooked is how disruptions in the Strait of Hormuz affect food markets as much as energy markets. Higher fuel and shipping costs can quickly ripple through agricultural supply chains, making imports more expensive for countries that are already vulnerable to food insecurity. This highlights why the economic consequences of regional conflicts can extend far beyond the immediate parties involved.

OneBlog Comment Creation Guide point that stands out is how the Strait of Hormuz functions as a bottleneck not only for energy exports but also for global food supply chains that depend on stable shipping routes. Even short-term disruptions can create ripple effects through higher transport costs and commodity prices, which are often felt most sharply by import-dependent developing economies.

One aspect that stands out is how the article connects the Strait of Hormuz disruption to both energy and food security, since higher fuel and shipping costs can quickly ripple through global supply chains. It would be interesting to explore which regions are most vulnerable to these secondary effects, especially countries that rely heavily on imported food and energy.

The article highlights an important point that often gets overlooked: disruptions in the Strait of Hormuz affect far more than oil prices. Because energy costs ripple through transportation, fertilizer production, and supply chains, even a temporary blockade can put additional pressure on global food security, especially in import-dependent economies.

One point that stood out is how the Strait of Hormuz functions as a bottleneck not only for energy markets but also for global food supply chains that depend on stable shipping routes. The article highlights how disruptions can quickly ripple far beyond the region, raising costs and uncertainty for countries with no direct involvement in the conflict. It would be interesting to see more discussion on which emerging economies are most exposed to prolonged shipping disruptions.

One of the most interesting points here is how the Strait of Hormuz functions as a bottleneck not only for energy markets but also for global food supply chains. The article highlights how regional conflicts can create ripple effects far beyond the Middle East, raising costs and increasing uncertainty for countries that depend heavily on imported fuel and agricultural inputs.

The article highlights an important point that often gets overlooked: disruptions in the Strait of Hormuz affect far more than oil markets. When a conflict constrains one of the world’s key shipping routes, the ripple effects can reach food prices, transportation costs, and inflation in countries far from the Gulf, making supply chain resilience a global concern rather than just a regional one.

One of the most important points here is that the Strait of HormBlog Comment Creationuz is not just an energy chokepoint but also a critical link in global food supply chains. Even short-term disruptions can create ripple effects through shipping costs, fertilizer markets, and food prices, especially for countries that rely heavily on imports. It would be interesting to explore which regions are most vulnerable to these secondary impacts.

What stood out to me is the connection between the Strait of Hormuz and global food markets, not just energy prices. When a key shipping route is disrupted, the effects can ripple through fertilizer supply chains, transportation costs, and ultimately food inflation in countries far from the conflict. It’s a useful reminder that geopolitical shocks often reach consumers through channels that aren’t immediately obvious.

The article highlights an important point that often gets overlooked: disruptions in the Strait of Hormuz affect far more than oil markets, with ripple effects reaching food supply chains and import-dependent economies around the world. It would be interesting to explore which regions are most vulnerable to prolonged shipping disruptions and how governments can strengthen resilience before temporary shocks become longer-term inflationary pressures.

One of the most important points here is that the Strait of Hormuz is not just an energy chokepoint—it also affects food supply chains through higher transportation and production costs. The article does a good job highlighting how a regional conflict can create global economic consequences, especially for countries that rely heavily on imported fuel and agricultural goods.

One point that stands out is how disruptions in the Strait of Hormuz can ripple far beyond energy markets and affect global food supply chains as well. The article highlights that even conflicts concentrated in one region can create wider economic consequences through shipping bottlenecks, which is a risk that often receives less attention than oil price movements. It would be interesting to see more discussion on which regions are most vulnerable to these secondary food-security impacts.

One aspect that stood out to me is how the Strait of Hormuz functions not only as an energy chokepoint but also as a critical link in global food supply chains. The article highlights how regional conflicts can create ripple effects far beyond the immediate area, raising questions about how countries can build greater resilience and diversify trade routes before disruptions become full-scale economic shocks.

One aspect that stands outBlog Comment Creation Guide is how the Strait of Hormuz affects far more than oil markets. When shipping through such a critical chokepoint is disrupted, the impact can quickly spread to food supply chains, transportation costs, and inflation in countries far removed from the conflict. It would be interesting to see more discussion on which regions are most vulnerable to these secondary economic effects.

A key takeaway here is that the Strait of Hormuz is not just an energy chokepoint but also a critical link in global supply chains, meaning disruptions can ripple into food prices and inflation far beyond the Gulf region. It would be interesting to explore how long-term uncertainty around the strait might accelerate efforts by countries to diversify trade routes and reduce dependence on vulnerable maritime corridors.

One of the most interesting points here is how the Strait of Hormuz functions as a bottleneck not just for energy markets, but also for global food supply chains that depend on stable fuel and shipping costs. The article highlights how a regional conflict can quickly create worldwideBlog Comment Creation Guide economic ripple effects, which raises important questions about how countries can build greater resilience into their trade and logistics networks.

One point that stood out is how the Strait of Hormuz functions as more than an energy corridor—it also indirectly affects global food systems through shipping costs and supply chain disruptions. The article raises an important reminder that even geographically concentrated conflicts can create inflationary pressure and economic uncertainty far beyond the region, especially for import-dependent economies.

One aspect that stood out is how the Strait of Hormuz functions not only as an energy chokepoint but also as a critical link in global food supply chains. Even temporary disruptions can create ripple effects far beyond the Gulf region, especially for countries that depend heavily on imported fuel andComment Creation Process agricultural inputs. It would be interesting to see more discussion on which emerging economies are most vulnerable to prolonged shipping restrictions.

The post highlights an important point: the Strait of Hormuz is not just an energy corridor, but a critical link in global supply chains that can affect food prices and economic stability far beyond the region. It would be interesting to explore how prolonged disruptions might accelerate efforts to diversify shipping routes and reduce dependence on a single maritime chokepoint.

One aspect that stands out is how the Strait of Hormuz affects far more than oil markets. When disruptions occur, the ripple effects can reach global food supply chains through higher transportation and fertilizer costs, which often put additional pressure on food-importing countries. It would be interesting to see more discussion on which regions are most vulnerable to these secondary impacts if the blockade persists.

The article highlights an important point that often gets overlooked: disruptions in the Strait of Hormuz affect not only energy markets but also global food supply chains through higher transportation and input costs. It would be interesting to see more discussion on how import-dependent developing countries can strengthen resilience when geopolitical shocks in a single chokepoint have such widespread economic consequences.

One of the most interesting points here is how the Strait of Hormuz functions as more than an energy chokepoint—it also affects global food supply chains through higher transportation and production costs. The article highlights how a regional conflict can quickly create worldwide economic ripple effects, especially for countries that depend heavily on imported fuel and food.

The post highlights an often-overlooked issue: disruptions in the Strait of Hormuz affect more than oil markets, they can also ripple through global food supply chains via higher transport and input costs. It would be interesting to explore which regions or import-dependent countries are most vulnerable if the blockade persists, since the economic impact could extend well beyond the immediate conflict zone.

One of the most interesting points here is how the Strait of Hormuz functions as more than an energy chokepoint—it also creates ripple effects across global food supply chains through higher transportation and production costs. It would be interesting to explore how long-term disruptions might accelerate efforts by importing countries to diversify both energy sources and trade routes to reduce this kind of vulnerability.

Pingback: O Choque de Ormuz, Descarbonização e os Minerais da América do Sul – Center for Macroeconomics and Development

Comments are closed.