Otaviano Canuto, Diogo Ramos Coelho, Bruno Saraiva

Policy Center for the New South, PP – 15/26, June 22, 2026

Global imbalances have returned to the center of international economic debate – and for robust reasons. Historically, large external imbalances and, more prominently, their corrections have been associated with financial crises, currency volatility, sudden reversals of capital flows, and geopolitical tensions. At the center of this debate is the commercial and financial relationship between the United States, China, and the rest of the world.

The debate over global imbalances gained centrality in the 2000s, when persistent U.S. current account deficits coexisted with large surpluses in economies like China, Japan, Germany, and oil-exporting countries. In that context, global imbalances were associated with the “recycling” of excess savings from surplus countries into the U.S. financial market.

Attention to the issue faded in the years following the Global Financial Crisis (2008–09), as current account imbalances narrowed relative to their pre-crisis levels. More recently, however, global imbalances have returned to the center of policy debates with greater focus on their composition, underlying drivers, and interaction with geopolitical fragmentation.

Basics of Global Imbalances

To understand the problem, one must start with a simple idea: when a country imports more than it exports, it needs to finance this difference with foreign resources. Imports and exports include the income accumulated by factors of production respectively brought in or sent abroad by the country.

The current account balance measures the net flow of goods, services, and income between a country and the rest of the world. It corresponds to the sum of the trade balance (net exports), net primary income (factor receipts from abroad minus payments to nonresidents), and net secondary income (current transfers, receipts minus payments) (IMF, 2026a).

Gross national disposable income is the sum of private and public consumption, private and public investment, and the current account. It is easy to see that the current account identity equals the difference between national saving and investment and establishes a link between domestic policies and external positions. That is why one may say that external deficits allow an economy to consume and invest more than it could with its own domestic production.

Alongside the flows recorded in the current account, the stock of external assets and liabilities evolves over time, reflecting both the accumulation of capital flows associated with persistent current account imbalances and valuation changes affecting existing positions. By the balance-of-payments identity, current account surpluses and deficits are jointly determined with capital and financial flows. Over time, these flows accumulate into changes in a country’s external asset and liability positions, while valuation effects arising from exchange rate and asset-price movements further alter the Net International Investment Position (NIIP).

A country running a current account deficit (an excess of domestic investment over saving) must finance this gap through net capital inflows. Conversely, changes in saving and investment behaviors across countries, as well as interest-rate shocks, generate capital flows that translate into corresponding changes in current account balances. These capital flows accumulate over time into the stock of external assets and liabilities, which comprise the NIIPs. Therefore, the NIIP equals the cumulative result of current and capital[1] accounts flows, and the effects of revaluation of foreign assets and liabilities.

Current account surpluses or deficits are not a problem per se. For instance, it is natural that rapidly growing economies finance part of their economic development with foreign capital. However, excessive imbalances, according to IMF methodology, arise when current account balances diverge from the norm that would be expected when accounting for structural fundamentals (development stage, demographics, natural resources), cyclical factors and desirable policies. As a result, excessive imbalances under the IMF framework are usually associated to distortive policies and have implications – domestically or abroad – in terms of levels of economic activity and jobs affecting the international and sectoral allocation of resources. For the same reason, excessive accumulation of net assets/liabilities may lead to concerns of unsustainability, sudden capital flows, and eventually bankruptcy. While the NIIP reflects a position of creditor or debtor to the rest of the world, gross positions may also indicate, by themselves, a robust or fragile external position if there are significant mismatches in terms of maturity, liquidity and yields. In sum, current account balances are flows, while the NIIP is a stock reflecting annual flows, valuation changes, and exchange-rate movements.

Waves of Global Imbalances

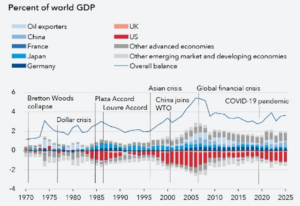

Global imbalances have unfolded in three distinct historical waves (IMF, 2026a) (Di Mauro & Zettelmeyer, 2026) (Figure 1):

- 1980s: U.S.-Japan tensions, which led to the Plaza Accord;

- Pre-2008: China-U.S. imbalances, which led to the global financial crisis;

- 2018-present: U.S. current account deficit; geopolitical fragmentation; systemic financial vulnerability.

Figure 1 – Global Imbalances Are Rising Again

Source: Gourinchas & Mumssen (2026)

In the 1980s, as one can see in Figure 1, a trade imbalance between the United States and Japan rose significantly. Tight monetary policy and large fiscal deficits in the United States led to high interest rates, as well as a sharply appreciated dollar, and a rising U.S. current account deficit. Japan, conversely, had persistent surpluses, driven by high savings and export-led catch-up growth. The trade imbalance morphed into a political discussion, as Japanese exports gained market share. Protectionist pressures grew as a result.

The Plaza Accord was signed aiming at correcting the dollar’s overvaluation. It is relevant to highlight two important aspects often misinterpreted in this context (Hoshi, 2026). While the Accord contributed to dollar depreciation, Japan’s current account surplus remained significant. In addition, it did not cause any subsequent downturn, as Japan went through high growth and asset price inflation in the late 1980s. Japanese stagnation came only after the burst of the asset bubble in the early 1990s. The Plaza Accord did not cause Japan’s “lost decades”, despite frequent claims to the contrary by critics of exchange-rate adjustments.

The Perfect Match in the 2000s

In the 2000s, the global economy exhibited a striking complementarity – like a perfect “match”. China consolidated itself as the world’s leading exporting economy, while the United States became the primary importer. China’s current account surplus (which encompasses trade, income, and services) rose from approximately $17 billion in 2001 to around $420 billion in 2008. During the same period, the U.S. current account deficit grew from about $394 billion to approximately $696 billion.

This “match” also occurred on the financial side. With export growth, surplus countries – China, Japan, Germany, and oil exporters – began accumulating massive dollar reserves. These savings needed to be invested somewhere. They flowed back primarily to the United States, through the purchase of U.S. Treasury bonds, which investors traditionally consider safe assets.

The United States financed both its external and fiscal deficits at relatively low cost, largely because it issues the world’s primary reserve currency. Persistent capital inflows from surplus economies, together with strong global demand for dollar-denominated assets, created unusually favorable financing conditions and helped keep long-term interest rates relatively low. This combination of abundant liquidity and inexpensive credit supported a prolonged expansion of household borrowing and rising real estate valuations. Subprime mortgages served as one of the principal channels through which abundant liquidity and easy credit reached households and the broader economy. The interaction between excess global savings, credit expansion, and housing finance ultimately fueled the U.S. housing bubble that preceded the global financial crisis.

The 2008 financial crisis, which began with the bursting of the U.S. housing market bubble, revealed how intertwined these financial and trade imbalances were, even if the surge in foreign capital inflows constituted only one of the factors underpinning the financial excesses of the preceding decade. The BIS (Bank for International Settlements) called attention to the role played by European banks operating in the United States – for instance Boryo and Disyatat ( 2011). These institutions raised short-term funds in the country and channeled them into purchasing assets tied to the local real estate market. A significant share of these transactions did not show up prominently in net balance of payments measures because the borrowing and lending activities of financial institutions largely offset each other. Yet the underlying gross flows and gross positions remained substantial, contributing to the buildup of financial vulnerabilities that net measures alone failed to capture.

In any case, when the housing bubble burst, the degree of interconnection between the global financial and trade systems became clear. The crisis quickly spread worldwide through banking markets, capital flows, and a widespread loss of liquidity and confidence.

Following the global financial crisis, the topic gained traction in G20 debates, particularly within the Framework for Strong, Sustainable and Balanced Growth, launched at the Pittsburgh Summit (2009). The goal was to promote multilateral monitoring of persistent deficits and surpluses, reduce systemic vulnerabilities, and encourage greater macroeconomic coordination among major economies. The IMF developed a framework to assess whether current accounts and exchange rates were out of sync to fundamentals, presenting annual “External Sector Reports” starting in 2012. Over time, however, the debate lost its centrality in the face of other crises and the relative stabilization of external imbalances during the 2010s.

For a time, some observers believed that the global financial crisis had partially corrected these imbalances. In recent years, however, concerns have resurfaced and returned to the center of policy debates.

The New Wave of Global Imbalances

Why are global imbalances back in the spotlight now? What has changed relative to previous waves?

As highlighted by the IMF in its latest World Economic Outlook, “global imbalances are widening after years of narrowing” (IMF, 2026b). But they do not look especially large yet. Figure 1 depicts global imbalances (the sum of all current surpluses, which is equal to the sum of all deficits plus a “global discrepancy”) at around 2% of global GDP, below the peak of almost 3% of global GDP observed prior to the global financial crisis, and above the trough of 0.4% of global GDP in 2019.

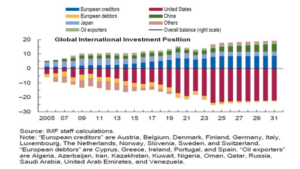

The geographical distribution of global imbalances has also not changed very much. The United States remains with the largest current account deficit relative to global GDP. On the surplus side, the group of main counterparts is also similar: the major economies – particularly the European Union, Japan, and China – alongside oil exporters.

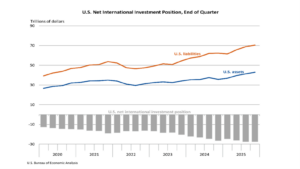

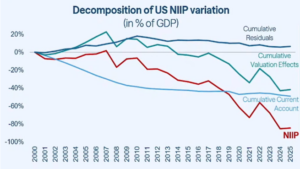

On the debtor side, the persistent current account deficit of the United States reflects the accumulation of external liabilities, although the relationship is not one-to-one owing to valuation effects (Balakrishnan, 2026). As a result, the United States’ NIIP reached about negative 90% of its own GDP (Figure 2) by end-2024. This can be understood not only as a result of sustained current account deficits but also because of sizeable valuation effects associated with rising U.S. equity prices – largely held by foreign investors – and an appreciating dollar. As highlighted by Gita Gopinath, a Harvard professor and former First Deputy Managing Director and Chief Economist of the IMF, at a lecture in the Bank of Atlanta on May 18 of this year, cumulative valuation effects have been higher as percentage of the U.S. GDP than cumulative current account deficits in the determination of such a decline of NIIP.

Since 2019, the U.S. NIIP has become much more negative because the country continued to run current account deficits and, because U.S. equity prices – especially large-cap technology stocks – rose much faster than foreign asset prices, increasing the value of foreign claims on the United States.

Figure 2, from the IMF World Economic Outlook of April, displays the peculiar evolution of the U.S. NIIP since the global financial crisis, while Figure 3a depicts the rise of the U.S. foreign liabilities relative to foreign assets (BEA, 2025). Figure 3b, in turn, taken from Gopinath (2026), matches current account and NIIP.

Figure 2

Figure 3a

Source: BEA (2025)

Figure 3b

Source: Gopinath (2026)

The deterioration of the U.S. external position stems largely from valuation effects rather than current account flows alone. Since the global financial crisis, rising U.S. equity valuations and the growing weight of U.S. financial assets in global portfolios have increased the value of foreign claims on the United States. As a result, a substantial share of the decline in the U.S. NIIP reflects financial valuation effects rather than trade deficits. This dynamic also reflects the persistent global demand for safe dollar-denominated assets, particularly U.S. Treasuries. In this context, U.S. Treasuries continue to play a central role as the primary safe asset of the international system, reinforcing global demand for liabilities issued by the United States.

Although the United States continues to accumulate high external liabilities, it still attracts extraordinary volumes of capital because global investors treat U.S. financial assets – especially Treasuries and U.S. corporate equities – as the primary instruments for store of value, liquidity, and safety in the international system. Under this logic, the U.S. current account deficit also reflects the very functioning of a dollar-centered international system, where the United States acts simultaneously as the primary issuer of safe assets and the main destination for global savings.

This distinction is important because it shifts the focus of the debate from trade flows to the structure of the international financial system. Part of the American political discourse – particularly among proponents of tariffs – argues that the U.S. trade deficit stems from unfair trade practices abroad, including currency manipulation, industrial subsidies, market-access restrictions, and other forms of state intervention. In this view, bilateral trade deficits, especially with China, represent the principal manifestation of global imbalances. Under this interpretation, tariffs, exchange-rate adjustments, and industrial policies become the main tools for restoring balance.

Yet this diagnosis sits alongside another feature of the U.S. economy: the persistence of large fiscal deficits and the U.S. role as balance sheet absorber of the world. While the U.S. government seeks to reduce the trade deficit, it continues to run substantial budget deficits that sustain domestic demand and require significant financing. At the same time, the U.S. deep and sophisticated financial system continues to attract financial flows that pay for but also stimulate current account deficits. This creates a tension between efforts to reduce trade imbalances through commercial policy and the continuation of fiscal policies that contribute to the underlying saving-investment imbalance.

If the U.S. external deficit also reflects its role as the world’s primary provider of safe assets, the issuer of the dominant reserve currency, and the main destination for global savings, then global imbalances cannot be understood solely through the lens of trade. They also emerge from the structure of the international financial system itself. Under this perspective, trade policy may influence the geographic distribution of deficits, but it is unlikely to eliminate the underlying forces that generate them.

What has changed compared to the past

Estevão & Fortun (2026) propose a redefinition of the role attributed to the United States:

“The old description of the United States as the world’s consumer of last resort captured an important part of export-led globalization, when U.S. household demand absorbed global production. It now needs to be broadened. The United States has also become the borrower of last resort, issuing the debt instruments that allow global savings to be recycled into dollar assets. Today even that description is too narrow. It is more accurate to say that the United States functions as the world’s balance sheet absorber of last resort.”

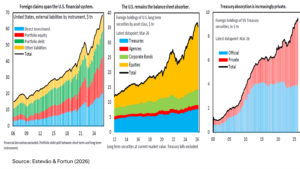

Figure 4 displays how foreign claims have expanded in the U.S. financial system, and how the United States operates as a “balance-sheet absorber”. It also highlights how the absorption of U.S. Treasuries has become increasingly private and, therefore:

“…more market based, and more responsive to rates, hedging costs, collateral needs, benchmark mandates, and risk appetite.”

Figure 4

The nature of the risk has also changed. In the 1980s, concerns centered primarily on exchange rates and trade imbalances between the United States, Japan, and Germany. In the pre-2008 period, a combination of debt-financed U.S. consumption and a continuous influx of foreign capital from surplus economies generated a different set of vulnerabilities. Systemic risks accumulated in the banking sector, mortgage markets, and highly leveraged household balance sheets. Unsurprisingly, the bursting of the subprime mortgage bubble in 2008 evolved into a global financial crisis.

Today, potential fragility appears less concentrated in household consumption and more embedded in the international financial architecture. The rapid growth of U.S. public debt, the world’s heavy reliance on Treasury markets, the expansion of Non-Bank Financial Intermediaries (NBFIs) – such as hedge funds and private credit funds (Canuto, 2023) – and the increasing concentration of U.S. equity markets in technology and AI-related firms have created a new set of systemic vulnerabilities.

This shift reflects the transformation described by Estevão and Fortun. As the United States increasingly functions as the world’s “balance-sheet absorber of last resort,” global savings no longer flow primarily into household borrowing and mortgage finance, as they did before 2008. Instead, they flow into Treasury securities, equity markets, and a growing ecosystem of financial intermediaries that channel and manage global capital. As Figure 4 illustrates, foreign claims on the U.S. financial system have expanded considerably, while private investors and market-based institutions have assumed a larger role in absorbing and intermediating these flows. As a result, the stability of the international financial system depends on the smooth functioning of Treasury markets, the resilience of NBFIs, and the sustained valuation of U.S. financial assets.

Another major difference from the pre-2008 period is that the main domestic counterpart to the U.S. external deficit is no longer household borrowing, but rather a combination of large fiscal deficits, rising public debt, and sustained capital inflows into U.S. financial markets, particularly technology and AI-related equities. The IMF projects a U.S. fiscal deficit of nearly 7.5% of GDP in 2026, while public debt exceeds 120% of GDP. At the same time, net U.S. external liabilities have reached approximately 24% of global GDP – a level significantly higher than that observed before the global financial crisis (Wolf, 2026).

In other words, the vulnerabilities associated with global imbalances have not disappeared; they have migrated. Before 2008, the main concern was the sustainability of household debt and mortgage finance. Today, concerns focus on the sustainability of public debt, the concentration of risk in market-based finance, and the possibility that a disruption in Treasury markets or a sharp correction in highly valued asset classes could transmit shocks across an international financial system that remains dependent on U.S. balance sheets.

The Fundamentals of Contemporary Imbalances: The Issue Goes Much Beyond Trade

The transformation of the United States into the world’s “balance-sheet absorber of last resort” carries important implications for the nature of contemporary global imbalances. The issue no longer revolves primarily around trade deficits or exchange-rate misalignments. Instead, it reflects the interaction between sovereign debt dynamics, financial market concentration, asset valuations, and geopolitical fragmentation. As a result, the international economy faces a new wave of global imbalances – one that may prove more fragile and more difficult to stabilize than previous episodes.

This shift also changes the focus of the debate. Rather than concentrating on bilateral trade balances, especially between the United States and China, analysts have examined the role of U.S. public debt, the demand for dollar-denominated assets, and the functioning of an international financial system that remains deeply dependent on U.S. assets.

In this context, the stability of the global economy has become increasingly dependent on the performance of U.S. financial markets. The concentration of equity valuations in a small number of technology and AI companies – the so-called Magnificent Seven now account for more than 30% of the S&P 500 – has heightened concerns about systemic risk (Canuto, 2025). Because global investors hold a large share of their wealth in dollar-denominated assets, a sharp correction in these markets would not remain a U.S. domestic event. It could rapidly transmit financial, liquidity, and confidence shocks throughout the international economy.

These developments highlight an important feature of contemporary global imbalances: the issue extends well beyond trade flows. Political debates often focus on bilateral trade deficits, particularly between the United States and China, and view tariffs as a natural response. Yet the experience of recent years suggests that tariffs have had a limited effect on the underlying drivers of imbalances. Rather than reducing Chinese value added embedded in U.S. imports, they have frequently redirected trade through third countries. Mexico, India, Vietnam, and other economies have acted as “connector countries,” importing Chinese inputs and intermediate goods and re-exporting final products to the United States.

In addition, tariffs do not directly address the macroeconomic and financial forces that sustain current account imbalances. Persistent U.S. fiscal deficits, the global demand for dollar-denominated assets, and the central role of U.S. financial markets as the world’s primary destination for savings continue to generate powerful incentives for capital inflows. As a result, trade restrictions may alter the geographic distribution of trade deficits without reducing aggregate external imbalances. IMF (2026a), di Mauro and Zettelmeyer (2026), and Gourinchas et al. (2026) all emphasize the limited ability of tariffs and industrial policies to address current account imbalances in the absence of broader macroeconomic adjustments.

One insightful theoretical framework for understanding this phenomenon is the Dominant Currency Paradigm (DCP), developed by Gopinath et al. (2020). The DCP challenges traditional trade models that assume international prices are set in either the exporter’s or the importer’s currency. Drawing on evidence covering approximately 91% of global trade, the authors show that most international transactions are invoiced in U.S. dollars, regardless of whether the United States participates in the transaction.

The core implications of the Dominant Currency Paradigm are:

- The bilateral exchange rate has a much smaller impact on trade flows than conventional models predict. What matters is the exchange rate of the dollar against all other currencies.

- A depreciation of the dollar does not produce the “expenditure switching” in the United States (the shift in consumption and demand from foreign products to domestic products following a currency devaluation) expected by conventional theories, as trade prices, fixed in dollars, do not change immediately.

- Tariffs and devaluations have much more limited effectiveness than their proponents assume.

- The dominance of the dollar in trade invoicing is structurally persistent, even if its share in global foreign exchange reserves has declined marginally.

In short: the United States continues to attract global savings; the dollar remains dominant; and U.S. markets continue to function as the primary repository of assets deemed “safe” in the international system. The U.S. external deficit, therefore, is not just a consequence of unbalanced trade, but also a byproduct of the functioning of a dollar-centered international financial system.

The paradox is that the very forces supporting U.S. financial dominance also amplify global systemic fragility. The growing concentration of savings, liquidity, and financial valuation in U.S. markets has left the rest of the world economy more exposed to U.S. asset cycles – U.S. sovereign debt dynamics, the role of NBFIs, tech/AI equity valuation cycles, and private credit.

Global Risks and Geopolitical Fragmentation

The U.S. imbalance conditions are aggravated by structural imbalances in other major economies – particularly China – and by geopolitical fragmentation. After all, trade, finance, and protectionism are deeply intertwined. Global imbalances do not result solely from excess consumption and debt in the United States, but also from the persistence of economic models reliant on high savings, trade surpluses, and a dependence on external demand in creditor economies.

China provides an illustrative example. The weight of household consumption remains relatively low – around 40% of GDP, compared to over 65% in the United States. As a result, China maintains high levels of domestic savings. For years after the global financial crisis, the real estate sector absorbed much of this savings surplus. As that cycle weakened, capital flowed toward industrial and manufacturing capacity, especially in strategic sectors. Given the relative insufficiency of domestic demand, a significant share of Chinese manufacturing capacity has once again become dependent on foreign markets.

In 2025, China’s trade surplus in goods reached a record US$1.2 trillion, while its current account surplus amounted to roughly US$735 billion (about 3.5 percent of GDP), according to the World Bank. These surpluses reflected not only the competitiveness of Chinese manufacturing, but also the structural difficulty of converting high domestic savings into domestic consumption. As a result, a significant share of Chinese production continued to depend on foreign demand.

In the current context of imbalances, the main surplus countries remain the same as in the pre-2008 period –China, Germany, Japan, and oil exporters – while the United States remains the primary net borrower of global savings. The problem is that these imbalances have begun to interact directly with geopolitical rivalry, industrial competition, and protectionist pressures. In U.S. politics, anti-China rhetoric represents a delayed reaction to the first “China shock” – the effects of China’s rapid integration into the global economy in the 2000s, which contributed to the loss of manufacturing jobs in the U.S. economy. Today, this legacy fuels resistance in the United States and other advanced economies toward Chinese advancement in higher value-added and advanced technology sectors, such as A.I., electric vehicles, and semiconductors.

At the same time, coordination among major economies has become more difficult. Disagreements between the United States and Europe over industrial policy, trade, technology controls, and economic security have complicated efforts to pursue common approaches to global economic challenges. The conflict in the Persian Gulf has added further uncertainty by increasing volatility in energy markets and reinforcing concerns about supply-chain resilience (Canuto, 2026). More broadly, the rise of strategic competition between major powers has weakened the cooperative environment that supported earlier efforts to manage global imbalances. Unlike previous periods, when policymakers could at least aspire to coordinated adjustment, governments today view economic policy through the lens of national security and geopolitical rivalry.

This shift carries important economic consequences. As countries place greater emphasis on resilience, strategic autonomy, and economic security, they increasingly rely on industrial policies, trade restrictions, export controls, investment screening mechanisms, and the reconfiguration of supply chains. While these measures may advance national objectives, they often do so at the cost of lower economic efficiency and higher production costs. The result is a global economy characterized by more expensive supply chains, reduced gains from specialization, and inflationary pressures. At the same time, fragmentation reduces the willingness of governments to undertake the coordinated macroeconomic adjustments needed to address global imbalances. This combination of persistent imbalances and weakening international cooperation raises the risk of a disruptive adjustment through trade tensions, financial instability, or slower global growth rather than through coordinated policy action.

In March 2026, a report prepared by a team led by Hélène Rey for the French G7 presidency (Bai et al., 2006) on the risks associated with contemporary global imbalances outlined what would be required for an orderly adjustment. There was relative academic consensus around five recommendations:

| Recommendation | Rationale / Degree of Consensus |

| United States: Reduce fiscal deficit | Broad consensus. The U.S. S-I (Savings-Investment) imbalance is a structural cause of the external deficit. |

| United States: Strengthen financial stability | Consensus. Regulating NBFIs and managing the Treasury market are urgent priorities. |

| China: Expand social spending and safety nets | Technical consensus, but politically difficult to implement. Reduces excessive precautionary savings. |

| European Union: Deepen capital markets integration | Consensus (Draghi Report). Would create a partial alternative to the dollar as a safe asset. |

| Preserve central bank independence | Unanimous consensus, including in reaction to pressures from the Trump administration on the Fed. |

An orderly adjustment would therefore require a simultaneous combination of U.S. fiscal consolidation, expansion of Chinese domestic demand, and greater European investment. Without some degree of macroeconomic coordination, the risk is that the system will continue to generate financial fragility, trade fragmentation, and rising political instability. In an environment of growing geopolitical fragmentation, however, it is difficult to assume that it will be possible to reproduce macroeconomic coordination mechanisms similar to those observed in earlier periods, such as the Plaza Accord or the post-2008 framework within the G20.

Final Considerations

Current imbalances have begun to interact with geopolitical rivalry, industrial competition, and economic fragmentation. In the United States, Donald Trump’s administration seeks to reduce the trade deficit through tariffs, export subsidies, and incentives for reindustrialization. At the same time, it maintains high fiscal deficits, including driven by defense expenditures boosted by geopolitical tensions, and a strong dependence on foreign capital, which limits its ability to reduce external imbalances.

The rivalry between the United States and China has also widened disputes over technology, supply chains, and economic security. Meanwhile, conflicts in Eastern Europe and the Persian Gulf increase uncertainty regarding energy, inflation, and trade. In times of tension, investors tend to seek assets deemed safe, further reinforcing the demand for dollars and U.S. government bonds.

Europe, for its part, still lacks sufficiently integrated financial markets to offer an alternative to the dollar as the primary destination for global savings. In China, the high level of precautionary savings, low domestic consumption, and an aging population continue to reinforce its dependence on investment, industry, and exports to sustain economic growth.

The report to the G7 French presidency pointed to a path toward an orderly adjustment: gradual reduction of U.S. fiscal deficits; strengthening of U.S. financial stability; stimulation of domestic consumption in China; deepening of European financial integration; and preservation of central bank independence. Moreover, the report suggested a plausible benign scenario in which unilateral actions in the right direction would set the incentives for others to act and contribute to a loosely (or implicitly) coordinated solution.

The trouble is that the world economy seems less capable of producing the minimum degree of political coordination necessary to implement these solutions. Moreover, the dollar-centered global financial system may tilt financial flows in a way that stirs global imbalances. In this sense, the IMF framework could be overlooking a key feature underlying global imbalances, which could mean that correction would require more than adjusting identified improper policies. The world remains integrated financially: the dollar remains dominant, capital flows remain gigantic and volatile, and markets remain interdependent. However, geopolitical rivalry, the absence of a recognized global leadership, protectionism, technological competition, and strategic fragmentation erode the mechanisms of cooperation that helped stabilize previous crises. Perhaps this is the primary tension of the contemporary international economy: financial globalization survives, but the political convergence that underpinned the economic order of recent decades seems fragile.

U.S. deficits (both public and trade) and financial markets continue to function as the primary anchor of international trade and the international financial system. At the same time, one must consider a deeper issue: the possibility that domestic U.S. politics may no longer support the stabilizing role historically associated with dollar hegemony and the economic order built post-1945. Unlike previous cycles, current imbalances are unfolding in an environment marked by strategic rivalry between the United States and China, domestic American political polarization, competition over industrial policies, geopolitical fragmentation, shocks in energy markets, the use of economic sanctions, and U.S. fiscal deterioration.

The international system remains integrated financially, but less capable of producing political coordination compatible with that level of economic integration. This tension perhaps constitutes the core structural dilemma of the contemporary international economy. The result is a world where globalization persists, but the convergence of the liberal order does not.

References

- BAI, Chong-En; GOPINATH, Gita; REY, Hélène; WEBER, Axel (2026). Paris Report 4: Global Imbalances and Financial Fragility. Prepared for the French G7 Presidency.

- BALAKRISHNAN, Ravi (2026). Global Imbalances: Current State and Scenarios for the Path Ahead, in Rey, H.; di Mauro, B. & Zettelmeyer (eds.), The New Global Imbalances – Paris Report 4, CEPR.

- BoE – Bank of England (2026). Rethinking Global Imbalances: Drivers, Risks, and Policy Priorities, Staff Discussion Paper, March.

- BEA – U.S. Bureau of Economic Analysis (2025). U.S. International Investment Position, 2nd Quarter 2025, September 29.

- BERNANKE, Ben (2005). The Global Saving Glut and the U.S. Current Account Deficit. Sandridge Lecture, Virginia Association of Economists.

- BORIO, Claudio & DISYATAT, Piti (2011). Global imbalances and the financial crisis: Link or no link? BIS Working Papers No 346, May.

- CABALLERO, Ricardo; FARHI, Emmanuel; GOURINCHAS, Pierre-Olivier (2017) The Safe Assets Shortage Conundrum. Journal of Economic Perspectives.

- CANUTO, Otaviano (2023). “Capital flows and emerging market economies since the global financial crisis”, in Gevorkyan, A. (ed.), Foreign Exchange Constraint and Developing Economies, Edward Elgar.

- CANUTO, Otaviano. (2024). China’s Economic Growth on Target Despite Challenges, Policy Center for the New South, April 17.

- CANUTO, Otaviano. (2025). The global economy is on a two-way track, Policy Center for the New South, PB – 47/25, October.

- CANUTO, Otaviano (2026). “Dire Strait of Hormuz: A Chokepoint for Global Food and Energy”, in Abdelhak BASSOU, Ferid BELHAJ, Ian O. LESSER, Marcus Vinicius de FREITAS, Rida LYAMMOURI, Otaviano CANUTO, Hafez GHANEM, Hinh T. DINH & Hugo A. MANSILLA. Hormuz and the Invisible Fractures: the Price of a Distant War – Views from the New South.

- Di MAURO, Beatrice & ZETTELMEYER, Jeromin (2026). “The New Global Imbalances: Why Care, Why Now, and What Can Be Done”, in Rey, H.; di Mauro, B. & Zettelmeyer (eds.), The New Global Imbalances – Paris Report 4, CEPR.

- DIHN, Hihn & CANUTO, Otaviano (2025). The Global Impact of President Trump’s Reciprocal Tariffs: Implications for Developing Countries, Policy Center for the New South, RP – 05/25, June.

- DU, Wenxin; KEERATI. Ritt Keerati & SCHREGE, Jesse (2025), Decoupling Dollar and Treasury Privilege, International Finance Discussion Paper, Board of Governors of the Federal Reserve System, December

- ESTEVÃO, Marcello & FORTUN, Jonathan (2026). The Balance Sheet Absorber, IIF – Institute for International Finance, May 28.

- GOPINATH, Gita et al (2020). Dominant Currency Paradigm. American Economic Review, vol. 110, no. 3.

- GOPINATH, Gita (2026). The Third Wave: Consequences of Global Imbalances. Presentation for the Federal Reserve Bank of Atlanta, May 2026. Available at: https://www.atlantafed.org/-/media/Project/Atlanta/FRBA/Documents/news/events/2026/05/17/financial-markets-conference/gopinath.pdf

- GOURINCHAS, Pierre-Olivier; REY, Hélène (2007). From World Banker to World Venture Capitalist: U.S. External Adjustment and the Exorbitant Privilege. In: Clarida, R. (ed.), G7 Current Account Imbalances, University of Chicago Press.

- GOURINCHAS, Pierre-Olivier & MUMSSEN, Christian (2026). Global Imbalances: Old Questions, New Answers? IMF Blog, April 6.

- GOURINCHAS, Pierre-Olivier; KINDBERG-HANLON, Gene; PATNAM, Mana; ROTUNO, Lourenzo; and RUTA, Michele (2026). Global Imbalances, Industrial Policy and Tariffs, IMF Working Paper WP/26/67, April.

- HOSHI, Takeo (2026). Global imbalances then and now: Lessons from the Plaza Accord, in Rey, H.; di Mauro, B. & Zettelmeyer (eds.), The New Global Imbalances – Paris Report 4, CEPR.

- IMF – International Monetary Fund (2026a). Understanding Global Imbalances, March.

- IMF – International Monetary Fund (2026b). World Economic Outlook, April.

- MILESI-FERRETTI, Gian Maria (2024). The U.S. Is the World’s Safe Asset Provider. Brookings Institution.

- MILESI-FERRETTI, Gian Maria (2026). The Return of Global Imbalances? The U.S. Case, in Rey, H.; di Mauro, B. & Zettelmeyer (eds.), The New Global Imbalances – Paris Report 4, CEPR.

- OBSTFELD, Maurice (2024). Global Imbalances Redux. Peterson Institute for International Economics.

- PETTIS, Michael (2020). Trade Wars Are Class Wars. Yale University Press.

- RAJAN, Raghuram (2010). Fault Lines: How Hidden Fractures Still Threaten the World Economy. Princeton University Press.

- REY, Hélène (2013). Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence. Jackson Hole Symposium, Federal Reserve Bank of Kansas City.

- REY, Hélène; Di MAURO, Beatrice & ZETTELMEYER, Jeromin (eds.) (2016). The New Global Imbalances – Paris Report 4, CEPR.

- WOLF, Martin (2026). The New Global Imbalances Are Becoming Dangerous. Financial Times.

- WORLD BANK (2025). China Economic Update: Navigating Uncertainty. December 2025. Washington, DC: World Bank.

[1] Note that according to the IMF BPM6, the capital account is usually a small component of the Balance of Payments, and includes only non-financial, non-produced asset transactions and capital transfers between residents and non-residents.

Otaviano Canuto, based in Washington, D.C, is a former vice president and a former executive director at the World Bank, a former executive director at the International Monetary Fund, and a former vice president at the Inter-American Development Bank. He is also a former deputy minister for international affairs at Brazil’s Ministry of Finance and a former professor of economics at the University of São Paulo and the University of Campinas, Brazil. Currently, he is a senior fellow at the Policy Center for the New South, a professorial lecturer of international affairs at the Elliott School of International Affairs – George Washington University, a nonresident senior fellow at Brookings Institution, and a professor affiliate at UM6P, and principal at Center for Macroeconomics and Development

Diogo Ramos Coelho is a Brazilian career diplomat and author. Since joining the Brazilian Foreign Service in 2010, he has worked on international economic, trade, and climate policy issues in Brasília, Washington, D.C., Mexico City, and at the International Monetary Fund. He has served as an advisor to Brazil’s Ministers of Finance and of Planning and Budget and is the author of two books, published in 2014 and 2024, on the global financial crisis and the crisis of the liberal international. His work focuses on international political economy, finance, trade, and global governance.

Bruno Saraiva is a civil servant at the Central Bank of Brazil), having worked at the Ministry of Finance (2004-06), the World Bank (2006-07) and the Inter-American Development Bank (IDB) (2007-11). He was head of the Department of International Affairs at the Central Bank of Brazil (2011-16), alternate director for Brazil at the International Monetary Fund (IMF) (2016-24) and is currently at service at the Brazilian Ministry of Finance.