Policy Center for the New South, Research Paper RP 07-25, 19 August 2025

1 Introduction

The international monetary system has been fully dominated by the U.S. dollar since the Second World War. The dollar hegemony cut across the end of the dollar exchange standard established by the Bretton Woods Agreement, and the dollar emerged from the global financial crisis—and the euro-area crisis—even stronger than before. The euro area and China are taking steps to strengthen the international role of their currencies, but attaining the fundamental strength of the dollar cannot be taken for granted.

This paper starts with an overview of the factors underlying the dominance of the U.S. dollar, meaning that any ‘de-dollarization’ is bound to be partial and limited, before delving into two areas where competitors to the dollar-based system have raised their profiles: the rising use of local currencies in cross-border payments between China and other countries, and the role played by the euro and the renminbi (RMB) in cross-country financial safety nets.

2 ‘De-dollarization’: Partial and Limited

Recent initiatives and policy moves by China and other countries to extend the use of the renminbi in the international monetary system, in the context of a slight shrinking in relative terms of the U.S. dollar share in global reserves, have sparked discussions about a hypothetical ‘de-dollarization’ of the global economy.

Directly or indirectly, the United States is by far the major supplier of safe and liquid assets to the rest of the world. It is the issuer of the major currency used for trade invoicing, the monetary policymaker with the strongest transmission abroad, and the main lender of last resort.

These attributes are self-reinforcing. The dollar’s presence in trade invoicing makes it more attractive to borrow in dollars, which in turn makes it more desirable to price in dollars. The U.S. role of lender of last resort makes it safer to borrow in dollars, which in turn increases the responsibility of the United States in times of crisis. All these gravitational factors consolidate Washington’s special position as the ‘sun’ around which the world’s currency system orbits.

The heavy financial sanctions imposed on Russia by the United States and its allies in Europe and Asia since the invasion of Ukraine, have sparked speculation that the weaponization of access to reserves in dollars, euros, sterling, and yen could fragment the international monetary order[1]. China, the argument goes, would tend to strengthen its own international payments system and accelerate the establishment of the RMB as a rival reserve currency, in order to reduce vulnerability in case of moves of a similar nature against it. Countries facing geopolitical risks in their relationships with the U.S. and Europe could seize the opportunity to switch out of the dollar system. It is not surprising, therefore, that the ‘de-dollarization’ of the global economy, ‘multipolarity’ or ‘bipolarity’ of the international monetary system, have become buzzwords. However, the gap between ambition and reality remains quite large.

2.1 Currencies as Means of payment

First, it is necessary to consider the difference between using a currency to settle transactions—that is, as a means of payment—and its role as a store of value. The use of a particular currency in transactions tends to lead to the amassing of reserves in that currency by central banks, which need to be ready for those payments.

However, it is worth distinguishing between the use of currencies for payments (flows) and stores of value (stocks, reserves), not least because transactions may be settled without using a store of value. A Brazil-China agreement signed-off in 2023, for instance, allows importers to make payments in local currencies, with settlements happening periodically. A similar scheme was inaugurated in 1982 by Brazil and other Latin American countries to economize on the use of U.S. dollars in all individual cross-border transactions between them (the ‘Agreement on Reciprocal Payments and Credits’). Brazil left in April of 2019, with obligations remaining until 2026.

It should be noted that the bulk of foreign exchange transactions are financial operations, not trade in goods and services. This means that the size and scale of Chinese foreign trade is a giant basis for the potential use of its currency, but not on the financial transaction side. In 2015, when the RMB was approved as part of the special basket of currencies that serves as the base for the Special Drawing Rights (SDR, the accounting currency issued by the International Monetary Fund), along with the dollar, euro, yen, and sterling, it was because of its weight in relation to China’s foreign trade, not because of its use in financial transactions.

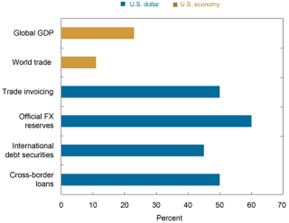

The global use of the U.S. dollar in the international monetary system is much greater than the relative size of the US economy (Figure 1). The dollar’s shares of foreign trade invoicing, international debt issuance, and cross-border lending, are well above what the U.S. shares of international trade, international bond issuance, and cross-border borrowing would suggest.

Figure 1: The U.S. Dollar’s Role in International Monetary System Eclipses the U.S. Presence in the Global Economy

Source: Ozge Akinci, Gianluca Benigno, Serra Pelin, and Jonathan Turek, ‘The Dollar’s Imperial Circle’, Federal Reserve Bank of New York Liberty Street Economics, March 1, 2023, https://libertystreeteconomics.newyorkfed.org/2023/03/the-dollars-imperial-circle/.

Trade can, of course, stimulate trade finance in a country’s currency. Lenders extend credit to facilitate the cross-border movement of goods and services.

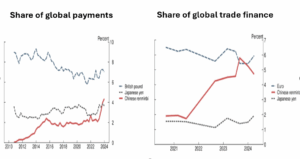

The RMB’s share of trade finance has more than doubled since Russia’s full-scale invasion of Ukraine. The RMB’s share by value of the market rose from less than 2% in February 2022 to 4.5% a year later (Figure 2). That reflected the use of China’s currency to facilitate trade with Russia, and the rising cost of dollar financing since the start of the Fed’s ongoing interest-rate hikes[2]. The RMB share of global trade finance is likely to continue to grow, notwithstanding the uncertainties about China’s growth outlook[3]. The rise of the RMB share of global trade finance from 2021 onward saw it overtake the euro’s share in 2023, when it reached nearly 6% of trade settlement, a near-tripling from September 2020, and above the euro share of 5.3% in 2023. The positions switched back in 2024, but still the RMB’s ascent since 2021 has been notable.

Figure 2: Share of Global Payments and Trade Finance

Note: U.S. dollar and euro shares of global payments are not shown but were 22.8% and 47.0% respectively in January 2024. The dollar share of global trade finance is not shown but was 84.1% in April 2024.

Source: Bastian von Beschwitz. Internationalization of the Chinese renminbi: progress so far and outlook, FEDS Notes. Washington: Board of Governors of the Federal Reserve System, August 30, 2024, https://doi.org/10.17016/2380-7172.3592.

The RMB’s rising share of trade finance reflects China’s drive to accelerate the internationalization of its currency. It constitutes a challenge to the West’s use of sanctions to bar major Russian financial institutions from using the Brussels-based Swift payments platform. The RMB’s rise among trade finance currencies has not been matched by greater use in international payments made via Swift, and the RMB’s share has plateaued at about 2% of the global total.

China already sought to internationalize the RMB in the years leading up to August 2015, when a devaluation led to severe capital flight. The People’s Bank of China (PBOC), China’s central bank, consequently decided to backtrack and impose draconian capital controls that stalled China’s progress in promoting the RMB’s global use. However, the PBOC seems to have shifted back to RMB internationalization since the beginning of 2022, by searching for greater use of the currency in the settlement of cross-border commodities trades, and improving global access to derivatives tied to RMB assets.

2.2 Currencies as Stores of Value

Central banks must have reserves of currencies with which they can operate in the various exchange transaction areas. The reason is simple.

Over the last few decades, more or less two-thirds of the world’s foreign reserves have been in U.S. Treasuries and other quasi-sovereign U.S.-dollar assets. A gradual decline in the dollar’s share in total reserves occurred in the 2000s, and was interpreted as a natural diversification by central banks, reflecting trade and financial globalization. However, not even the introduction of the euro, despite high expectations at the time, changed the dollar’s dominance in foreign reserves substantially. Dollar dominance persisted despite the falling share of U.S. GDP in the global economy. In fact, just as the end of convertibility into gold in the early 1970s consolidated rather than diminished its predominant role, so the financial crisis of 2007-08 led to an increase in the dollar’s presence in banking and non-banking transactions. Only lately have trends started to change.

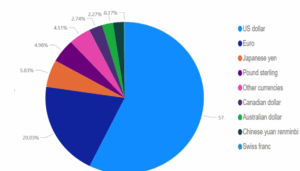

The first quarterly IMF report of data on official foreign exchange reserves of 2025 shows a reduction in the degree of dollar dominance. Since the beginning of the century, the dollar’s share of central bank reserves has fallen by twelve percentage points, from 71% in 1999 to 57.3% in 2024 (Figures 3a and 3b).

Figure 3a: Official Foreign Exchange Reserves by Currency (U.S. Dollar, Billions)

Source: IMF COFER. https://data.imf.org/en/Dashboards/COFER%20Dashboard

Figure 3b: Allocated Currency Reserves (Billions)

Source: IMF COFER. https://data.imf.org/en/Dashboards/COFER%20Dashboard

This decline in the dollar’s dominance has not worked in favor of sterling, the yen, or the euro, despite the latter’s rise in its first decade of existence. Instead, ‘non-traditional reserve currencies’ (Australian dollar, Canadian dollar, Swiss franc, and others), including the renminbi, have benefited[4].

At the end of 2024, non-U.S. central banks held $6.47 trillion in dollar-denominated assets, such as U.S. Treasury securities, U.S. corporate bonds, and U.S. mortgage-backed securities. Even though the dollar’s share has dropped since 2014, holdings of dollar assets rose from $4.4 trillion in 2014 to $7.1 trillion in Q3 2021, before falling as the Fed initiated quantitative tightening (QT) and interest-rate hikes[5].

2.3 De-dollarization Will Remain Slow and Bounded

Four gravitational factors favor the continuation of the dollar’s central position in international financial markets, in trade invoices and payments, and in public and private foreign exchange reserves. Economies of scale and of scope in the different uses of a currency tend to reinforce its advantages relative to others once it reaches a certain share—something the literature calls “network – complementarity and synergy – effects”[6]. The relative expansion of the other currencies depends on how successfully they manage to offset those factors, as they tend to reinforce the dominance of the most-used currency.

First, the scale and scope of dollar-denominated transactions favors the continuity of the dominant position of the U.S. currency. The increase in liquidity and the reduction in transaction costs—including because of technological improvements of platforms—in non-traditional foreign exchange markets, such as the Australian and Canadian dollars and the RMB, have reduced their disadvantage relative to the U.S. dollar despite the ‘network effects’ in favor of the latter, but only to a limited extent.

Second, no other monetary system offers an equivalent volume of investment-grade government bonds as the United States. That volume allows central banks to accumulate reserves and private investors to use them as a ‘haven’, something reinforced by the QE employed for over a decade by the Fed after the global financial crisis. In this regard, the announcement in July 2012 by then President of the European Central Bank, Mario Draghi, that the ECB would do “whatever it takes” as a last-resort provider of liquidity for euro-denominated assets issued in the euro area was significant. Furthermore, a European Recovery Fund was created in 2020. The global supply of liquid and safe-haven assets usable as central bank reserves has since tended to widen in favor of the euro, mitigating its relative disadvantages relative to the dollar.

Third, non-traditional currencies were for a time favored by a partial search for returns in reserve management. The central bank balance sheets of advanced and emerging economies have taken on enormous proportions in the new millenium[7]. Some of these banks separate what would be the appropriate tranche for ‘liquidity management’ (the reason why there are reserves in liquid and low-risk assets, with the purpose of stabilization) from the ‘investment tranche’ (possible to be allocated in less-liquid but more profitable assets). Many countries have also created Sovereign Wealth Funds (SWFs) to manage the investment tranche of the public sector’s foreign currency holdings. The search for diversification has favored the use of non-traditional reserves.

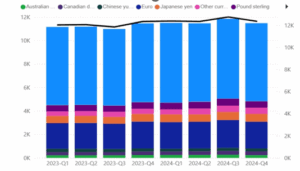

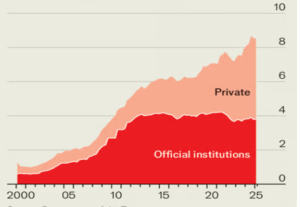

It should be noted that, over the last decade, a rising share of the demand for dollar assets has come from sources other than central banks, including government pension funds, life-insurance companies, and other private financial institutions (Figure 4)[8]. The investment tranche in the acquisition of assets abroad has been on the rise.

Figure 4: Foreign Holdings of U.S. Treasuries (Trillions)

Source: The Economist (2025), based on U.S. Treasury Department.

The fourth gravitational force in favor of the dollar is the absence of U.S. regulations restricting liquidity and asset availability, including capital controls. Despite the sanctions already applied in cases such as Iran, Venezuela, and Russia, there is a difficulty for Chinese bonds compared to U.S. Treasuries and the other three major currencies (euro, yen, and sterling).

Since the global financial crisis, China has sought to extend the use of the RMB in international trade and as a reserve asset at other central banks. This was followed by a proliferation of foreign-exchange swap lines with other countries (as discussed below). However, while trade transactions and reserves held by central banks and other global public investors may reinforce the renminbi’s position as an alternative currency to the dollar, euro, yen, and sterling, the qualitative leap toward the internationalization of the Chinese currency as a reserve currency will only occur when confidence in its convertibility is sufficient to convince unofficial (private) investors to hold reserves denominated in it[9]. It is not by chance that currency swap lines activated with China have been little used, while those with the Federal Reserve have been activated in times of need to stabilize flows.

By all indications, Chinese financial authorities do not appear to be considering relinquishing capital controls as a priority in the short term. They will likely expand the use of the RMB to the extent that it can be done without relinquishing controls and, therefore, without the ambition of building a parallel regime or substituting for the existing one. The reserve issuer must accept that large amounts of its currency circulate in the world and, therefore, that foreign investors have some weight in determining domestic long-term interest rates and the exchange rate.

In 2022, right after Russia’s full-scale invasion of Ukraine, portfolio foreign capital movements into and out of China were illustrative of what is at stake, and the potential costs for China of a rushed exit from its current regime. Data released by the Institute of International Finance (IIF) in March 2022 revealed an unprecedentedly large outflow of portfolio (debt and equities) capital from China[10].At the same time, such flows remained stable in other emerging economies.

Although later partially reversed, the timing of the phenomenon suggests that it had some correlation not with domestic difficulties with China’s property sector (or other domestic issues), but mainly with the war in Ukraine and Western sanctions on Russia. Paradoxically, the same sanctions that stimulated the rise of the RMB in transactions also sparked capital movements out of China. Given the magnitude of repressed domestic financial wealth in China, one may guess that dramatic outflows would follow that capital-account liberalization in search of diversification, as happened in 2015.

2.4 Can the US Dollar’s ‘Exorbitant Privilege’ be a ‘Handicap’?

In the 1960s, then French finance minister Valéry Giscard d’Estaing coined the term “exorbitant privilege” to describe the U.S. dollar’s position as the dominant currency. Such a position allows a country to supply cash or safe assets needed by the rest of the world in exchange for goods and services or long-term assets, and consequently to benefit from lower interest rates than would be the case otherwise.

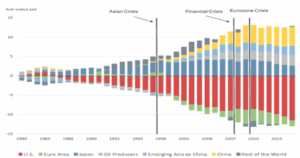

Country-level mismatches between supply and demand for safe assets appear in the evolution of net stocks of safe foreign assets. Figure 5 portrays the U.S. and euro area below the line, as safe-asset providers, while China, Japan, oil producers, and emerging Asia (excluding China) are net purchasers above the line. To the extent that the world stock of safe assets moves upward, cross-border net purchases of safe assets give carriers of the exorbitant privilege greater amounts of goods and services and investment assets from the rest of the world, in exchange for those safe assets[11].

Figure 5: Net Safe Positions as a Fraction of World GDP

Source: Ricardo J. Caballero, Emmanuel Farhi and Pierre-Olivier Gourinchas, Global Imbalances and Policy Wars at the Zero Lower Bound, Harvard, 16 January 2020. https://scholar.harvard.edu/sites/scholar.harvard.edu/files/farhi/files/glob_imbalances_011620_pog.pdf

There are those, however, who see that ‘bonus’ as onerous. This depends on whether the goods and services and investment assets ‘imported for free’, corresponding to a certain level of current- and/or capital-account deficit that the issuer of safe assets can incur in exchange for the provision of those assets, come in addition to, or replace, local production, regardless of whether the safe-asset provider runs a surplus or deficit in the other balance-of-payment accounts.

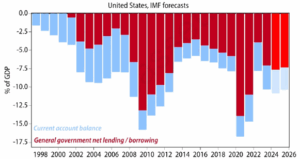

The ‘onerous’ view of the exorbitant privilege is presented, for instance, by Michael Pettis, for whom many of the world’s economies use a portion of U.S. demand for goods to offset deficient domestic demand and fuel domestic growth. As a counterpart, the U.S. economy must then rebalance by increasing its household or fiscal debt[12] (Figure 6):

“Without the widespread use of the US dollar as the mechanism that allows global imbalances to be absorbed by the US economy, these imbalances cannot exist.”

Figure 6: U.S. Current Account and Government Borrowing

Source: Gavekal, Where will the excess dollars go?21 April 2025.

Excessive or insufficient current-account balances are better approached through the IMF’s current-account imbalances evaluation methodology, relative to countries’ fundamentals, in its annual external sector reports[13]. The exorbitant privilege should not be confounded with countries’ occasional shortcomings in obtaining full employment, or efficient allocation of resources.

In sum, notwithstanding the ongoing drive by countries—China in particular—for a greater variety of major currencies in the international monetary system, de-dollarization will most likely be partial and limited. For such a transformation to take place more rapidly and at a deeper level, a metamorphosis of China’s regulatory and policy regime would be needed, which China most likely does not have the desire to implement at the current historical juncture.

While the euro has remained mostly a regional reserve currency, the U.S. may retain its exorbitant privilege through the provision of U.S. dollar-safe assets for longer—provided, of course, that dramatic portfolio reshuffles out of U.S. dollar assets, as in the episode of U.S. ‘reciprocal tariffs’ of April 2, 2025, do not take place, and that U.S. public debt does not enter any unsustainable trajectory[14]. A drive for a greater share of euro assets in global portfolios seems poised to take place—a speech by Christine Lagarde, ECB president, at the end of May 2025 outlined an agenda of what would it take to get there[15]. In any case, a trend has started toward diversification as a response to heightened U.S. sovereign and credit risks on what used to be thought of as risk-free assets[16].

3 Increasing Use of Local Currencies in Cross-Border Payments

In March 2023, Brazil and China agreed to use their currencies in bilateral trade. China is Brazil’s largest trading partner, being the destination of more than 30% of Brazilian exports and the origin of more than 20% of imports. Given the trend towards surplus flows on the Brazilian side, it is assumed that Brazil will accumulate reserves in RMB if all bilateral trade transactions become covered by the agreement.

At the August 22-24, 2023, BRICS summit in Johannesburg, the leaders of Brazil, Russia, India, China, and South Africa said they wanted to use their national currencies more for cross-border payments, which are currently dominated by the U.S. dollar and other global convertible currencies. Like China and the other BRICS, several countries have also sought to develop alternative external payment mechanisms. Pairs of countries have agreed to settle commercial and financial transactions with each other in their local currencies, usually facilitated through bilateral agreements between their central banks.

National governments might want to use local currencies in cross-border payments, instead of convertible and fully usable currencies, to avoid becoming subject to geopolitically motivated sanctions by those countries that issue the dominant international currencies and that are destinations for external reserves in their currencies. Russia, Iran, and Venezuela are such cases in the recent past. China and others are clearly also looking to reduce their vulnerability to potential sanctions.

Additionally, one can point to an eventual gain in terms of lower stocks of reserves in fully convertible currencies—dollar, euro, yen, sterling—necessary for central banks to ensure stability in their cross-border payments. In this case, however, it is worth noting a possible cost of bilateral cross-border payment using local currencies: in bilateral relations, in which a country has a systematic surplus, it tends to accumulate foreign reserves in the currency of the country on the deficit side, instead of doing so in a currency that is fully convertible and generally accepted by other agents in foreign-exchange markets.

It is enough for one side to impose the use of local currency in payments so that, even against their will, the private agents of the other must accept it to make a transaction possible. Brazilian exporters, for example, now no longer face mandatory convertibility of their foreign revenues into Brazilian currency, and can dispose of their revenues in dollars or however they wish. But if the Chinese demand payment in their currency, Brazilians will have no other option if they want to sell there. That has not been the case so far, and apparently no bilateral Brazil-China transactions have been executed yet under the 2023 agreement on local-currency use.

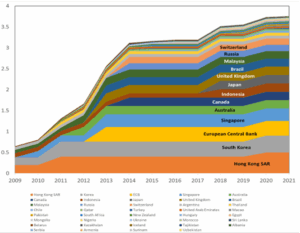

There is also another sphere in which the RMB has seen great expansion: bilateral swap lines between central banks. By the end of March 2023, the PBOC had signed bilateral agreements for the creation of currency swaps with the central banks of 41 other countries, amounting to $480 billion, and with the balance of funds activated via such lines reaching $15.6 billion (Figure 7). Some of these bilateral swap lines have not been extended – like the one with Brazil. But in addition to such credit swap lines, China has also expanded offshore clearing banks.

Figure 7: Evolution of PBOC Swap Lines (RMB Trillions)

Source: Hector Perez-Saiz and Longmei Zhang, Renminbi Usage in Cross-Border Payments: Regional Patterns and the Role of Swaps Lines and Offshore Clearing Banks, IMF Working Paper WP/23/77, March 2023.

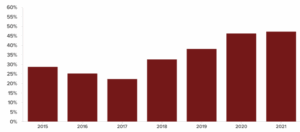

China has been able to use its currency to settle half of its foreign trade and investment transactions (Figure 8). The median use of the RMB went from zero in 2014 to 20% in 2021, based on a sample of external payments between China and 125 other countries[17].

Figure 8: RMB Share of China’s Total Cross-Border Settlements

Source: Hung Tran, Understanding the growing use of local currencies in cross-border payments, Atlantic Center, Econographics, 25 August 2023. https://www.atlanticcouncil.org/blogs/econographics/understanding-the-growing-use-of-local-currencies-in-cross-border-payments/

Furthermore, the RMB has occasionally been used in bilateral transactions between third parties. Some refineries in India used RMB to buy oil from Russia. Argentina resorted in August 2024 to its bilateral line with China to pay its debt service with the IMF[18].

It is also worth following an ongoing project to develop a digital multi-currency platform that is being implemented by the central banks of China, Hong Kong, Thailand, and the United Arab Emirates (UAE), and which was initially supported by the Bank for International Settlements (BIS)[19]. Digital currencies from China and the others may become usable for external payments in a plurilateral framework.

Russia and India have also been looking to extend the use of their currencies. Meanwhile, at a meeting of the Association of Southeast Asian Nations (ASEAN) in May 2025, in Indonesia, members agreed to develop a framework for the settlement of external transactions in their local currencies.

The BRICS installed in 2010 an Interbank Cooperation Mechanism to facilitate payments in local currencies by the group’s banks[20]. In 2018, it launched BRICS Pay, a public-private partnership project for a digital payment platform in local currencies[21].

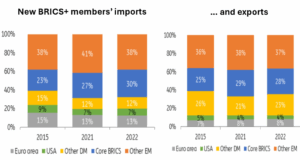

The August 22-24, 2023, BRICS summit included an invitation to six countries to join the group: Argentina (which declined the invitation), Ethiopia, Egypt, Iran, Saudi Arabia, and UAE. Given that the original BRICS have increased their share of new members’ exports and imports (Figure 9), the use of local currencies will rise if bilateral agreements between them and China are also signed.[22]

Figure 9: Core BRICS Countries Have Gained Weight in New BRICS Members’ Trade

Source: ING Economic and Financial Analysis, BRICS Expansion: The Saudi Surprise Adds Momentum To The De-Dollarisation Debate, 24 August 2023. https://think.ing.com/articles/brics-expansion-the-saudi-surprise/

In sum, pairs of countries have agreed to settle commercial and financial transactions with each other in their local currencies, usually facilitated through bilateral agreements between their central banks. China has been able to use its currency to settle half of its foreign trade and investment transactions. The growing use of local currencies in external payments will be part of the “slow and bounded de-dollarisation”.[23] A partial fragmentation of the global payments system is underway.

4 Lines of External Financial Defense[24]

4.1 International Reserves are the First Line of External Financial Defense

A country’s international reserves are its first line of defense[25]. Holding international reserves is costly, as these assets provide low returns. Their non-use to obtain alternative types of assets corresponds to an opportunity cost, which is in principle justified by the gains from protection against shocks and stoppage of transactions. A very hard-to-answer question is what the optimal levels of reserves is, in order to maintain a balance between such costs and benefits[26].

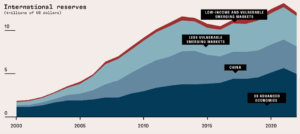

Countries’ international reserves have grown in volume, after a dip in the second half of the 2010s (Figure 10). However, the aggregate numbers hide a very variable picture among individual countries. Some 97% of those reserves have been accumulated by approximately 50% of countries, whereas around ninety emerging market and low-income countries account for the remaining 3% of reserves[27]. While many emerging market economies substantially increased their international reserves in the 2000s, that has not been the case for most low-income countries[28].

Figure 10: International Reserves

Source: Andrey Stanley. Global Financial Safety Net, IMF – Finance and Development, December 2023. https://www.imf.org/en/Publications/fandd/issues/2023/12/PT-global-financial-safety-net

4.2 Pooling Resources is the Second Line of Defense

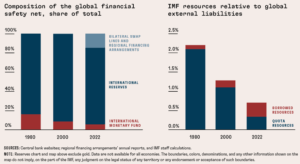

Pooling resources—via bilateral swap lines and regional or plurilateral arrangements—is an additional shield against shocks. Swap lines are arrangements that are designed to improve liquidity conditions and to help ease strain in financial markets. They support financial stability and serve as a prudent liquidity backstop (Figure 11).

Figure 11: Global Financial Safety Net

Source: Andrey Stanley. Global Financial Safety Net, IMF – Finance and Development, December 2023. https://www.imf.org/en/Publications/fandd/issues/2023/12/PT-global-financial-safety-net

The increased weight of this second line of defense can be illustrated by looking at the Federal Reserve and the ECB. The Fed operates dollar swap lines with the following central banks: Reserve Bank of Australia, the Bank of Canada, Danmarks Nationalbank, the Bank of England, the ECB, the Bank of Japan, the Bank of Korea, the Banco de Mexico, the Reserve Bank of New Zealand, Norges Bank, the Monetary Authority of Singapore, Sveriges Riksbank (Swedish central bank), and the Swiss National Bank. The highest dollar transaction through swap lines is with the ECB ($814 billion). The only emerging market with such a transaction is Mexico ($15 billion). Most swap lines were used during the COVID-19 pandemic

The Federal Reserve also operates foreign-currency liquidity swap lines with the Bank of Canada, the Bank of England, the Bank of Japan, the ECB, and the Swiss National Bank.

The ECB, meanwhile, is part of a swap-line network of standing bilateral arrangements with five other major central banks (the Bank of Canada, the Bank of Japan, the Swiss National Bank, the Bank of England, and the Fed). The ECB has increasingly used swap and repo lines since the 2008-09 global financial crisis.

The ECB provides euro against foreign currencies, which are accepted as collateral. Under reciprocal swap lines, the ECB may also receive foreign currency by providing euro as collateral. Under the repurchase agreements, the ECB provides euros to non-euro area central banks, and receives euro-denominated financial assets as collateral.

These swap and repo lines help meet the liquidity needs of euro and non-euro countries in order to prevent spillback effects that might have an adverse impact on the smooth transmission of the ECB’s monetary policy from impacting on euro-area financial markets and economies.

The ECB uses a strict set of criteria when deciding whether to grant swap and repo lines to non-euro area central banks. In June 2020, the ECB established a temporary Eurosystem repo facility for central banks (EUREP), which aims to broaden access beyond the swap and repo lines.

As shown by Figure 11, the second line of defense has emerged since the turn of the millennium. But like international reserves, swap lines are out of reach for many emerging market and developing economies (EMDEs). Also, the relative size of the IMF has diminished, including relative to global external liabilities (Figure 11, right panel).

EMDEs have instead tended to rely on piling up foreign-exchange reserves as a form of self-insurance. Self-insurance is neither individually nor collectively optimal, and this has prompted discussions about a more robust, multi-layered, global financial safety net.

Several EMDE central banks have swap lines with the People’s Bank of China (Figure 7), although the non-convertibility of the renminbi limits the value of these swap lines[29]. The template offered by China aims to facilitate bilateral trade and investment, rather than provision of a safety net. However, as we already noted, Argentina was able to utilize its currency swap line with China in 2023 to overcome difficulties in complying with its IMF debt service obligations.

Strictly speaking, since the global financial crisis, China has sought to extend the use of the renminbi in international trade and as a reserve asset at other central banks. It pursued a proliferation of currency swap lines with central banks in other countries, including Brazil.

4.3 The Role of the IMF as the Center of the Global Financial Safety Net Needs Boosting

The IMF provides the broadest and most general layer of defense against shocks, while—as discussed—countries differ very much in their ability to resort to first and second lines of defense. However, the IMF’s lending capacity as a share of global external liabilities has shrunk over time (Figure 11), and the share of borrowed resources has increased[30]. There remain weaknesses in the global financial safety net for EMDEs, particularly for those unable to accumulate large international reserves. These will remain subject to capital-flow and exchange-rate volatility, while the reliance on foreign currency credit will continue to be a source of vulnerability. There is therefore an overall need to strengthen the global financial safety net, by strengthening IMF liquidity provision and widening the financial safety net. Addressing capital-market volatility should also be pursued[31].

5 Conclusion

A multipolar international monetary system is not here yet. Notwithstanding the ongoing drive by some countries—China in particular—for a greater plurality of main currencies in the international monetary system, increasing the use of the renminbi, de-dollarization looks set to be partial and slow. A faster and deeper transformation would require a metamorphosis in China’s regulatory and policy regime, which the country most likely will not have the desire to implement at the current historical juncture. While the euro has remained mostly a regional reserve currency, the United States may retain its exorbitant privilege through the provision of U.S. dollar-safe assets for longer. On the other hand, there is a high likelihood that the euro area will implement a strategy of raising the profile of the euro as a reserve currency. The erratic and volatile policymaking that has prevailed in the U.S. tends to propel investors to speed up the diversification of their basket of means of reserving value.

In the meantime, pairs of countries have agreed to settle commercial and financial transactions with each other in their local currencies, usually facilitated through bilateral agreements between their central banks. China has been able to use its currency to settle half of its foreign trade and investment transactions. The growing use of local currencies in external payments will be part of the slow and bounded de-dollarisation. A partial fragmentation of the global payments system is underway.

Finally, the global financial safety net needs to be reinforced, especially in terms of its capacity to support EMDEs. As competitors to the dollar emerge, international investors may generate instability by switching to different parties in the multipolar system, exacerbating destabilizing speculation and leading to self-fulfilling confidence crises. It suffices to note the monetary instability in the years between the First and Second World Wars, when sterling and the dollar prevailed together. Reinforcing the existing facilities and expanding the financial capacity of the international organization at the center of the multilateral system—the IMF—as well as strengthening its support for decentralized arrangements, should be pursued.

The monetary system is on the way to losing its single polarity. The world should do whatever it takes to minimize the risks of instability that may rise during and after such a transition.

Otaviano Canuto, based in Washington, D.C, is a former vice president and a former executive director at the World Bank, a former executive director at the International Monetary Fund, and a former vice president at the Inter-American Development Bank. He is also a former deputy minister for international affairs at Brazil’s Ministry of Finance and a former professor of economics at the University of São Paulo and the University of Campinas, Brazil. Currently, he is a senior fellow at the Policy Center for the New South, a professor affiliate at UM6P, a professorial lecturer of international affairs at the Elliott School of International Affairs – George Washington University, and a nonresident senior fellow at Brookings Institution.

NOTES

[1] Otaviano Canuto, War in Ukraine and Risks of Stagflation, Policy Center for the New South PB – 18/22, March 2022, https://www.policycenter.ma/publications/war-ukraine-and-risks-stagflation; Jennifer Johnson-Calari, Arnab Das and Franco Passacantando, The “Weaponisation” of Money: Risks of Global Financial Fragmentation, IAI Papers 24/20, June 2024. https://www.iai.it/sites/default/files/iaip2420.pdf

[2] Hudson Lockett and Cheng Leng, Renminbi’s share of trade finance doubles since start of Ukraine war, Financial Times, 11 April2023. https://www.ft.com/content/6d5bbdbc-9f5d-41b2-ba80-7d8ac3973cf3

[3] Otaviano Canuto, The Third Plenum and China’s Economic Growth Challenges, Policy Center for the New South, 2 August 2024. https://www.policycenter.ma/publications/third-plenum-and-chinas-economic-growth-challenges

[4] Serkan Arslanalp, Barry J. Eichengreen and Chima Simpson-Bell, The Stealth Erosion of Dollar Dominance: Active Diversifiers and the Rise of Nontraditional Reserve Currencies, IMF Working Paper No. 2022/058, 22 March 2022. https://www.imf.org/en/Publications/WP/Issues/2022/03/24/The-Stealth-Erosion-of-Dollar-Dominance-Active-Diversifiers-and-the-Rise-of-Nontraditional-515150

[5] Otaviano Canuto, Quantitative Tightening and Capital Flows to Emerging Markets, Policy Center for the New South PB – 42/22, June 2022. https://www.policycenter.ma/sites/default/files/2022-06/PB_42-22%20%28%20CANUTO%20%29.pdf

[6] Serkan Arslanalp, Barry J. Eichengreen and Chima Simpson-Bell, The Stealth Erosion of Dollar Dominance: Active Diversifiers and the Rise of Nontraditional Reserve Currencies, IMF Working Paper No. 2022/058, 22 March 2022. https://www.imf.org/en/Publications/WP/Issues/2022/03/24/The-Stealth-Erosion-of-Dollar-Dominance-Active-Diversifiers-and-the-Rise-of-Nontraditional-515150

[7] Such a rise starting after the emerging market crises of the 1990s was approached by Otaviano Canuto and Matheus Cavallari, The Mist of Central Bank Balance Sheets, Policy Center for the New South PB-17/07, February 2017. https://www.policycenter.ma/publications/mist-central-bank-balance-sheets

[8] The Economist, How Trump might topple the dollar, 16 April 2025. https://www.economist.com/finance-and-economics/2025/04/16/how-trump-might-topple-the-dollar

[9] Otaviano Canuto, China’s Renminbi Needs Convertibility to Internationalize, Policy Center for the New South, 28 July 2021. https://www.policycenter.ma/opinion/china-s-renminbi-needs-convertibility-internationalize

[10] Robin Brooks, Jonathan Fortun and Jonathan Pingle, Global Macro Views: A Realignment in Global Capital Flows, Institute of International Finance, 24 March 2022. https://www.iif.com/Publications/ID/4726/Global-Macro-Views-A-Realignment-in-Global-Capital-Flows

[11] Otaviano Canuto, Climbing a high ladder: development in the global economy, Policy Center for the New South, 2021 (cap. 7). https://www.policycenter.ma/publications/climbing-high-ladder-development-global-economy

[12] Michael Pettis, Will the Chinese renminbi replace the US dollar?, Review of Keynesian Economics, Vol. 10 No. 4, Winter, pp. 499-512.

[13] IMF, External Sector Report 2025, July 2025 https://www.imf.org/en/Publications/ESR/Issues/2025/07/22/external-sector-report-2025

[14] Otaviano Canuto, The Spring of Tariff Regret, Policy Center for the New South, 5 May 2025, https://www.policycenter.ma/publications/spring-tariff-regret;

[15] Christine Lagarde, Earning influence: lessons from the history of international currencies, Speech at an event on Europe’s role in a fragmented world organized by Jacques Delors Centre at Hertie School in Berlin, Germany, 26 May 2025. https://www.ecb.europa.eu/press/key/date/2025/html/ecb.sp250526~d8d4541ce5.en.html.

[16] Hung Tran, The search for safe assets, Atlantic Council – Econographics, 6 June 2025 https://www.atlanticcouncil.org/blogs/econographics/the-search-for-safe-assets/

[17] Hector Perez-Saiz and Longmei Zhang, Renminbi Usage in Cross-Border Payments: Regional Patterns and the Role of Swaps Lines and Offshore Clearing Banks, IMF Working Paper WP/23/77, March 2023. https://www.elibrary.imf.org/view/journals/001/2023/077/article-A001-en.xml

[18] Xiaofeng Wang and Otaviano Canuto,. The Dollar-Renminbi Tango: The Impacts of Argentina’s Potential Dollarization on its Relations with China, Policy Center for the New South PB – 39/23, October https://www.policycenter.ma/sites/default/files/2023-10/New_PB_39-23_Xiaofeng%20Wang%20and%20Otaviano%20Canuto.pdf

[19] BIS, Project mBridge: connecting economies through CBDC, 26 October 2022. https://www.bis.org/publ/othp59.htm. The BIS has recently left https://www.reuters.com/business/finance/bis-leave-cross-border-payments-platform-project-mbridge-2024-10-31/

[20] BRICS 2022 China, The BRICS Interbank Cooperation Mechanism Annual Meeting & Financial Forum 2022 Held in Beijing, 30 June 2022. https://brics2022.mfa.gov.cn/eng/zdhzlyhjz/others/202208/t20220826_10754259.html

[21] BRICS Pay https://www.brics-pay.com/

[22] On the evolution of BRICS, see Otaviano Canuto and Bruno Saraiva, BRICS in Times of Tectonic Shifts, Policy Center for the New South PP – 26/25, July 2025. About the relationships between their financial institutions and the Bretton Woods sisters (IMF and World Bank), check Pepe Zhang, Otaviano Canuto, and Fernando Straface, From Bretton Woods to Braided Path: Navigating MDB Dynamics Amid Global Shifts, CEBRI Journal, Jan-Mar. 2025.

[23] Otaviano Canuto The U.S. dollar’s “exorbitant privilege” remains, Policy Center for the New South PB – 21/23, April 2023.

[24] Otaviano Canuto and Amshika Amar, Emerging Markets and Developing Economies in the Global Financial Safety Net, Policy Center for the New South PP – 01/24, February 2024. https://www.policycenter.ma/publications/emerging-markets-and-developing-economies-global-financial-safety-net

[25] Alina Iancu; Seunghwan Kim and Alexei Miksjuk, Global Financial Safety Net—A Lifeline for an Uncertain World, IMF – Chart of the Week, 30 November 2021. https://www.imf.org/en/Blogs/Articles/2021/11/30/global-financial-safety-net-a-lifeline-for-an-uncertain-world

[26] Bruno Saraiva and Otaviano Canuto, O. (2009). Vulnerability, Exchange Rate and International Reserves: Whither Brazil? Center for Macroeconomic Development, 21 September 2009. https://www.cmacrodev.com/vulnerability-exchange-rate-and-international-reserves-whither-brazil/

[27] Andrey Stanley. Global Financial Safety Net, IMF – Finance and Development, December 2023. https://www.imf.org/en/Publications/fandd/issues/2023/12/PT-global-financial-safety-net

[28] Otaviano Canuto and Matheus Cavallari, The Mist of Central Bank Balance Sheets, Policy Center for the New South PB-17/07, February 2017. https://www.policycenter.ma/publications/mist-central-bank-balance-sheets

[29] Otaviano Canuto, Rising Use of Local Currencies in Cross-Border Payments, Policy Center for the New South, August 2023. https://www.policycenter.ma/publications/rising-use-local-currencies-cross-border-payments .

[30] Andrey Stanley. Global Financial Safety Net, IMF – Finance and Development, December 2023. https://www.imf.org/en/Publications/fandd/issues/2023/12/PT-global-financial-safety-net

[31] UN – United Nations (2023). Our Common Agenda Policy Brief 6: Reforms to the International Financial Architecture, May. https://www.un.org/sites/un2.un.org/files/our-common-agenda-policy-brief-international-finance-architecture-en.pdf