BRICS in Times of Tectonic Shifts[1]

Policy Center for the New South PP – 26/25

Otaviano Canuto and Bruno Saraiva

1. Introduction

When, sixteen years ago, the leaders of Brazil, Russia, India, and China gathered in Yekaterinburg to form the BRICs group, it felt as though reality was imitating fiction—or more precisely, that a piece of geoeconomic analysis from an investment bank had materialized into reality (O’Neill, 2001). Today, the BRICS (South Africa joined the original four soon after) has become BRICS+, including five other emerging economies (Egypt, Ethiopia, Indonesia, Iran, and the United Arab Emirates)[2]. BRICS+ encompasses nearly half of the world’s population, accounts for almost 40% of global GDP (in purchasing power parity, or PPP), and represents one-fourth of global trade and foreign direct investment.

The idea of bringing together developing countries to influence international forums and organizations is not new. In the post–Second World War era, it dates back at least to the Non-Aligned Movement, the Group of 77 at the UN, and the G24 within the Bretton Woods institutions. What sets the BRICS apart, however, is that it was not merely an effort to unite lower-income countries to influence a world dominated by wealthy powers in a Cold War context. Instead, it marked the moment when countries with growing economic weight came together to claim a prominent role in the post-Cold War global economic order. It is no coincidence that the first BRICS summit took place after the 2008–09 global financial crisis—an event from which these countries emerged relatively unscathed, unlike the advanced economies of the Global North, where the crisis originated[3].

In this brief, we evaluate the scenarios projected by the study that followed the original BRICs concept note (Wilson and Purushothaman, 2003), assess the current positioning of BRICS+, and briefly discuss the main challenges the group faces.

- From Invention to Reality

The investment bank article that coined the BRICs term, by Jim O’Neill, sought to challenge the G7-led global economic governance structure by highlighting the rise of major emerging economies as a decisive factor in forming a new, more representative global arrangement (O’Neill, 2001).

While the Bretton Woods financial architecture was forged in the immediate post-war environment, formal coordination between the major global economic powers emerged in the mid-1970s in the wake of the oil shock and the collapse of the post-war fixed exchange rate system. The G7 evolved from informal gatherings of finance ministers on the margins of International Monetary Fund-World Bank meetings into a standalone summit of heads of state and government—the G20 would later follow a similar path, albeit more slowly. In any case, the original agenda of the G7, like that of the G20, was primarily economic: to foster global economic cooperation, defend free trade, promote rapprochement with socialist economies, and coordinate positions on the ongoing reform of the international monetary system.

Although the G7 included Russia in the late 1990s—forming the G8—this arrangement did not survive Russia’s annexation of Crimea, after which G7 countries imposed sanctions and excluded Russia from the group. On the other hand, the 2008–09 global financial crisis, while not leading to an expansion of the G7, contributed to two significant developments in global governance:

- Elevation of the G20 to a summit-level forum of heads of state and government; and

- Formation of BRIC (soon expanded to BRICS) as a platform for coordination and cooperation among emerging economic powers.

The G20 was initially created largely as an initiative by advanced economies to ‘educate’ emerging economies—particularly in fiscal and regulatory policies—after the financial contagion from the Asian and Russian crises of the previous decade had exposed deep financial linkages between the two groups. The later elevation to the level of heads of state occurred in a context in which the financial crisis originated in advanced economies, prompting them to call on emerging economies to play a greater role—including financially—in multilateral activities.

Over these sixteen years, BRICS has served as an important platform for emerging economies to push for reform of the IMF’s quotas and governance (2010), and capital increases for the World Bank (2010 and 2018). Additionally, the group created two institutions of its own: the New Development Bank (NDB) and the Contingent Reserve Arrangement (CRA), which now form part of the global network of multilateral and regional development banks and financial safety nets. In the past two years, five new members have joined BRICS; others may follow in the near future. Perhaps even more important is the sheer size and growth potential of these emerging economies. However, questions remain about the group’s effectiveness and relevance in global economic governance[4].

- Time Travel: How BRICS Has Evolved Compared to the Original Projections

This section compares the evolution of the BRIC economies (Brazil, Russia, India, and China) with the projections made in a 2003 article by Dominic Wilson and Roopa Purushothaman (W&P), focusing on assumptions related to growth and exchange rates. Their projections used a simple Cobb-Douglas model of real growth, with labor force growth rates based on demographics, investment based on recent averages, and productivity convergence occurring at an annual rate of 1.5%.

The higher growth potential of lower-income economies stems from their lower capital intensity (and hence higher returns), and their ability to adopt technologies developed in advanced economies—a phenomenon known as ‘catch-up’. While W&P’s projections extended to the year 2050, this analysis will focus on the horizon through 2025. It’s worth noting that one complication in the global investment dynamic is that the rise of these emerging economies meant that the world’s largest economies by GDP would no longer necessarily be its wealthiest in terms of per-capita income.

Some of W&P’s main market-price GDP projections for the period included:

- China would overtake France and the UK by 2005, Germany by 2007, and Japan by 2016;

- India would overtake Italy in 2016, France in 2019, and both the UK and Germany by 2023;

- Russia would overtake Italy in 2019 and France in 2024; and

- Brazil would overtake Italy only in 2025.

Additionally, the combined GDP of the four BRIC countries was projected to reach half the size of the G6 (excluding Canada) by 2025, and China was expected to reach half the size of the U.S. economy by 2023. Two-thirds of this convergence was to come from higher real growth, and one-third from currency appreciation.

Naturally, long-term projections are subject to a range of potential errors. Even small inaccuracies in estimated growth parameters can lead to significant differences over time. The scenarios assumed growth-friendly policies (with their absence possibly causing major distortions), and assumed that shocks would not alter trends fundamentally, rather causing only temporary deviations that would self-correct[5]. Moreover, one-third of the projected relative gains were expected to come from currency appreciation, based on structural determinants—assuming rising productivity would cause nominal exchange rates to converge toward purchasing power parity (PPP) rates.

To assess the actual performance of these economies since 2000, we need to consider not just how much they have grown, but also the differentiated impacts of two major global shocks: the 2008-09 global financial crisis (which lingered in Europe until 2012–13), and the COVID-19 pandemic from 2020 to 2022. In addition, Brazil experienced a domestic crisis between 2015 and 2016, while Russia faced disruption following its invasions of Crimea (2014) and Ukraine (2022), and the resulting international sanctions.

According to the IMF’s World Economic Outlook database, the relative performance of the BRIC group—using market-price GDP converted at current exchange rates—was as follows: China did indeed overtake France, the UK, and Germany between 2005 and 2007, as projected, and overtook Japan in 2010—six years ahead of schedule. India also outperformed expectations, overtaking Italy in 2015, France in 2019, and the UK in 2021. It is projected to surpass Japan in 2025. Brazil and Russia overtook Italy earlier than expected (2010 and 2012, compared to the 2025 and 2019 projections, respectively). However, the crises in Brazil and Russia allowed Italy to regain its position, which is projected to persist at least until 2030, according to IMF forecasts.

While Brazil and Russia underperformed relative to the original projections, their average real growth between 2000 and 2024 (2.4% and 3.4%, respectively) still exceeded that of the G6 economies (only the U.S. came close, with a 2.2% average). This growth differential was expected but ultimately insufficient to close the gap with the world’s most advanced economies.

The other convergence mechanism—structural appreciation of emerging market currencies—played a smaller role than anticipated. Brazil’s real effective exchange rate appreciated nearly 90% between 2003 and 2011, but then fell by 43% through 2020. Russia’s ruble nearly doubled in value between 2000 and 2013, only to fall 28% over the next three years, and it hasn’t regained a consistent upward trend. India’s currency offered little help (a real effective appreciation of just 10% from 2000 to 2020, with values fluctuating since). China saw a 39% real appreciation between 2000 and 2015, followed by a 12.5% depreciation.

A different story emerges when using purchasing power parity (PPP) to compare these economies[6]. By this metric, BRIC convergence with the G6 is indisputable. On a PPP basis:

- China overtook Japan in 2001 and the U.S. in 2016;

- India overtook Germany in 2005 and Japan in 2009;

- Russia became larger than France, the UK, and Italy between 2003 and 2004, and larger than Germany and Japan in 2021.

- Brazil was larger than Italy, the UK, and France between 2008 and 2010.

Moreover, the combined PPP GDP of the four BRIC countries surpassed that of the G6 in 2019.

Although the BRIC group represented about 20% of the global economy at the start of the century, their more dynamic growth meant they contributed more than 30% to global growth on average from 2000 to 2004. As their global economic share rose and their growth rates outpaced that of advanced economies, their contribution to global growth rose to 44% on average for the first quarter of the twenty-first century (excluding the global recession years of 2009 and 2020). In contrast, the G6’s contribution declined from over 20% at the turn of the century to an average of 17.5% for the entire period.

In summary, comparing the actual performance of the BRIC group over this first quarter-century to Goldman Sachs’s original projections reveals:

- China and India not only fulfilled but exceeded expectations, while Russia and Brazil were hampered by idiosyncratic economic shocks;

- Currency appreciation played a smaller role than anticipated in speeding up convergence;

- The combined economic weight of the BRIC group, measured in PPP, now exceeds the G6’s by 22%, and is projected by the IMF to be 43% larger by 2030; and

- The BRIC countries have become crucial engines of global growth.

Clearly, the economic dimension of BRICS—now expanded to include 10 countries—goes far beyond what was envisaged in the original coinage of the acronym. BRICS nations now play a significant and growing role in global trade, are important sources and destinations for foreign direct investment (even though such flows are still dominated by advanced economies), have accumulated massive foreign reserves, lead global commodity markets (especially in food and energy), hold strategic reserves of critical minerals for the digital economy, and—particularly in China’s case—dominate advanced technology niches.

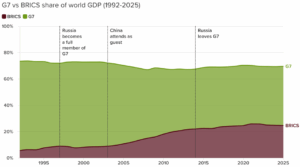

Figure 1 shows the rising share of the original BRIC countries in world GDP in PPP terms. While the G7 corresponded to 63% of world GDP in 1992, and now corresponds to 44%, the founding BRIC members’ share has more than doubled to close to 25%.

Figure 1

Source: Atlantic Council, Seven charts that will define Canada’s G7 Summit, June 12, 2025.

On the other hand, BRICS countries remain highly heterogeneous in terms of culture, politics, and institutions, and they face a wide range of economic challenges in their development paths. Notably, economic integration among BRICS members remains relatively weak; most maintain more substantial and complex economic relationships with G7 countries. Several BRICS members also face the so-called ‘middle-income trap’, when demographic pressures and labor market transformations arrive before the countries achieve income levels comparable to those of advanced economies.

- The Macroeconomic Context of the Emergence of BRICS

When BRICS was formed a decade and a half ago, the global financial crisis seemed to signal a structural realignment of the world economy, as if the financial meltdown in core advanced economies was creating the space needed for emerging markets to rise. On one hand, BRICS symbolized this reconfiguration, while on the other, it grouped together economies that benefited from a virtuous global demand cycle in which the United States played the role of ultimate consumer, and China served as a major supplier of inexpensive manufactured goods and a buyer of food and intermediate goods.

At the same time, the U.S. helped sustain global demand through substantial fiscal and current account deficits, while China emerged as the world’s primary saver, helping finance these deficits and accumulating large foreign exchange reserves, mostly in U.S. Treasury bonds. This arrangement contributed to low inflation, modest interest rates, intense capital flows (albeit volatile), currency appreciation in emerging markets (though at times excessive), and a long commodity boom cycle.

The period following the crisis represented the peak of this model, but also marked the beginning of its unraveling. The macroeconomic debate at the time raised new questions—or at least old questions in new forms—reshaping certain alliances. Expansionary monetary policies in advanced economies, including quantitative easing, sparked debate about spillover effects, and led emerging market economies to implement capital flow management tools to protect themselves from surges of volatile capital.

The conversation also turned toward more effective micro- and macroprudential regulation and financial supervision, aimed at addressing existing vulnerabilities and preventing new ones from emerging in the financial system.

Meanwhile, timid fiscal responses in some advanced economies focused attention on the challenge of sustaining global demand. Here, the U.S. aligned with certain emerging markets to call for more proactive countercyclical fiscal policies in major economies to help stabilize and balance global demand.

All this amplified a topic that had already been gaining traction in U.S. policy circles before the crisis: global current-account imbalances. While the U.S. benefited from absorbing global savings and accessing cheap consumer goods, it also became increasingly concerned. The growing negative net international investment position and rising public debt led the U.S. to push global imbalances to the top of the multilateral agenda[7].

This debate often veered into accusations of currency manipulation, as some argued that surplus economies were not allowing their currencies to appreciate and were hence preventing the rebalancing of flows. In this respect, BRICS held a somewhat constructive position: only two of its economies—China and Russia—had surpluses, while Brazil, India, and South Africa were in deficit. Moreover, the latter three had allowed significant currency appreciation during the first fifteen years of the century. More importantly, the contribution of emerging markets to global economic growth has increased substantially throughout the twenty-first century.

Ultimately, BRICS emerged at a historical moment characterized by multifaceted debates and shifting groupings, depending on the issue. There was hope that a truly multilateral system would prevail in global economic relations. However, the second half of the 2010s steered the global economy in another direction.

- BRICS in a World Moving East and Toward a New Polarization

The notion that multilateralism was working against U.S. interests has gained traction in U.S. politics. More significantly, the perception of China as a rising superpower—and thus the U.S.’s main economic rival—has become dominant. This perspective was solidified during the first Trump administration and has persisted beyond 2020. As a result, the theme of geoeconomic fragmentation has remained central in multilateral macroeconomic discussions. In the ongoing trade war, the second Trump U.S. administration continues to target China with heavy-handed measures[8].

As noted above, this first quarter of the twenty-first century has confirmed the economic rise of China—and, to a lesser degree, India—as an undeniable historical reality. However, this rise has occurred within a model in which the U.S. remains the economic and financial center, and the dollar is by far the world’s dominant international currency Canuto, 2023d). While the turbulence being seen in early 2025 has its own specific triggers, it should not be seen as a singular event, but rather as part of an ongoing process likely to cause further disruption in the years ahead.

What is new is that the U.S. administration now appears unwilling to continue playing the leadership role it held in the post-Second World War multilateral order. Instead, it is attempting to force adjustments in trade partner behavior, generally through targeted barriers designed to prevent China from assuming global economic leadership. The coming years are likely to be marked by intense rivalry between the current superpower and the rising one—a situation that poses risks (and possibly some opportunities) for the global economy. Historically, adjustments of this magnitude have often been traumatic. This is a very different context from that in which BRICS was originally conceived.

This new polarization raises key questions for BRICS members. How can BRICS avoid becoming just another pawn in a high-stakes geopolitical chess match? What opportunities exist for BRICS members to pursue their own agendas without being forced to take sides in the U.S.–China rivalry?

At first glance, greater global economic fragmentation or polarization serves none of the BRICS members well. Even China prefers not to provoke a direct confrontation with the U.S. Instead, it is seeking more time to consolidate its economic strength before challenging U.S. leadership in global economic governance. This makes sense, given the importance of the U.S. market and the central roles played by its financial system and currency. As is well known, issuing the world’s reference currency gives the issuer an ‘exorbitant privilege’, but it also entails responsibilities that China may not be ready—or willing—to take on at this stage[9]. For now, the current system still benefits China.

For the rest of the group (perhaps excluding Russia and Iran), deeper economic fragmentation is likely to be highly detrimental, even if it offers a few short-term advantages. Greater fragmentation tends to lower global growth potential, increase costs, and hinder international trade[10]. Given the vast gap in size and power (both economic and military) between the two superpowers and emerging market economies, the best course of action is to avoid aligning too closely with either pole. As the Swahili proverb says, ‘when elephants fight (or make love), it is the grass that suffers’.

So, what role can BRICS play in helping to prevent a new polarization and creating a better environment for emerging markets? A promising path would be to defend and strengthen multilateralism, while promoting cooperation on issues and in ways that do not fuel polarization or global conflict. This approach will be explored further in the next section.

- Challenges to Advancing a BRICS+ Agenda

BRICS aims to be a diplomatic platform with a predominantly economic focus, though its scope extends far beyond that, encompassing global security, the environment, health, agriculture, social policy, and more. Our focus here, however, is on the BRICS financial track, which involves the finance ministries and central banks of member countries and their respective agendas.

The BRICS work in the financial track follows three main lines of action:

- Coordinating common positions to present in multilateral forums, particularly in support of reforming the governance of the Bretton Woods institutions (IMF and World Bank);

- Promoting initiatives and creating institutions to expand the reach of member countries (the NDB and CRA are the most prominent examples, but many other smaller initiatives are also underway)[11]; and

- Encouraging technical cooperation and knowledge-sharing to strengthen domestic policies.

Below are some illustrative areas in which the BRICS financial track could evolve in the current context:

6.1. BRICS+ as a Global South Leader in the Multilateral Debate

Reforming global economic governance—especially the Bretton Woods institutions—was a founding goal of BRICS and is a demand that dates back decades. However, this is not a fully harmonious issue within the current expanded composition of BRICS, given the differences between members and their occasionally divergent interests. Still, BRICS is well-positioned among emerging markets to lead the push for more representative governance of multilateral financial institutions. This role can be played by pursuing inclusive agendas that naturally attract the support of a broad majority of emerging markets and developing economies (EMDEs). BRICS can—and should—aspire to be the voice of developing countries, advocating for a more representative economic order and greater resources for the global financial safety net and multilateral development banks (MDBs), including more funding to address climate change. One potential flagship initiative BRICS could champion is the sale of a portion of the IMF’s gold reserves to support higher levels of concessional lending and expanded technical assistance[12].

When countries face external financial shocks, they need financial buffers to weather them. The global financial safety net refers to the set of institutions and arrangements that provide these layers of defense. From any given country’s perspective, there are three main lines of defense: international reserves, pooled resources (such as swap lines and multilateral financing arrangements), and the IMF (Canuto & Amar, 2024). Expanding and easing access to the IMF—the most critical layer—is essential.

6.2. Expand Membership and Deepen the Role of the NDB

The New Development Bank (NDB) is the most significant achievement of BRICS over the past 15 years[13]. With $50 billion in capital and a membership that extends beyond the original BRICS countries, the NDB is a key source of development financing and part of the multilateral development bank community. One major challenge for the NDB is how to expand its membership and make broader use of local currencies in its lending. Additionally, as an institution with a growing technical capacity and institutional structure, the NDB could serve as a platform for hosting other BRICS initiatives.

6.3. Improve the CRA

The Contingent Reserve Arrangement (CRA) was launched alongside the NDB and pools $100 billion in reserves from the original five BRICS members for mutual support. The central banks of CRA members have developed its operational framework and conducted tests to ensure functionality. However, the CRA has never been activated. As a reserve-sharing mechanism among countries that do not issue reserve currencies, the CRA must be perceived by all participants—not just potential borrowers—as enhancing their defenses. A complicating factor is that only China and Russia (among current CRA members) have accumulated reserves through current account surpluses. The other countries have accumulated reserves through active policies aimed at reducing external vulnerability—at considerable cost, which needs to be offset by the additional security the CRA provides[14].

In the current CRA design, access to funds is, to some extent, tied to IMF adjustment programs, hence the relatively low cap for funds available without an IMF program. This creates a trade-off: a lower non-linked limit means more security for reserve-lending countries but less usefulness for borrowing countries. One way to raise this non-linked limit would be to strengthen the CRA’s monitoring and conditionality mechanisms—essentially replicating some IMF functions[15]. However, this could impose high costs on members and deepen the divide between creditor and borrower countries within the CRA. In the current conditions, it might be more feasible to explore the use of local currencies (a complex change) and to expand the CRA’s membership and capacity without altering its core model.

6.4. The ‘BRICS Currency’ Agenda and Alternatives

There is growing consensus within BRICS that the international monetary system needs reform to become more secure, impartial, and efficient, serving the interests of developing economies. The weaponization of the dollar in recent years, with the increasing use of unilateral sanctions (without UN approval), has fueled this discussion. Since the Johannesburg Summit (2023), BRICS has advocated greater use of local currencies in transactions between members[16]. One possible step forward would be to create a network of bilateral local currency agreements, similar to the Local Currency Payment System (SML, from the Portuguese and Spanish names) used in Mercosur. However, even between Brazil and Argentina, which established an SML in 2008, the system has been used mostly for Brazilian exports and has not surpassed $1 billion annually—while Brazil’s exports to Argentina have averaged around $15 billion in recent years. This is a delicate issue—not only because of the economic implications, but also because of geopolitical sensitivities—and BRICS members should approach it with great caution, especially in an already tense global environment.

6.5. Promote Infrastructure Investment

This could involve mobilizing the savings and investment capacity of certain BRICS members to support infrastructure development in others. Ongoing discussions suggest creating platforms or mechanisms to facilitate such investments. China’s Belt and Road Initiative (BRI) demonstrates the potential for increasing infrastructure investment flows, especially in light of the growing need for sustainable infrastructure amid climate change pressures. While the BRI offers valuable lessons, the Chinese model is not replicable—nor should it be—given the debt-related issues it has caused in many low-income countries[17].

- Conclusion: How to Navigate a Complex and Likely Prolonged Geoeconomic Transition

In this brief, we have shown that BRICS, as a geoeconomic reality, has neither disappointed nor fully met the expectations set at its inception. As a project aimed at increasing the strength and voice of the Global South in global economic debates and arrangements, BRICS will increasingly need to navigate very complex dynamics.

First, China’s economic size relative to the other BRICS members—though similar to the disparity between the U.S. and other G7 members—poses some additional challenges. The G7 was formed in the context of established U.S. global leadership and deep economic integration among its members. In contrast, BRICS brings together a more heterogeneous group of countries, including a subordinate economic superpower whose rise is likely to trigger turbulence as the global geoeconomic and geopolitical order adjusts.

It is also worth questioning to what extent the middle-income trap will present serious challenges to BRICS countries. Historical experience with late transitions to high-income status shows that the most successful model has been export-oriented growth. However, that model now faces increasing constraints—particularly in a world in which the largest economy is actively working to reduce its trade deficits. On top of this, BRICS countries are confronting major structural challenges, including global warming, aging populations, and transformations in the world of work—before they have even reached high-income status. Therefore, despite the vast economic potential of emerging markets, the obstacles ahead are significant.

Moreover, the current U.S. administration’s confrontational stance toward China complicates efforts by BRICS countries to pursue a common agenda without drawing U.S. attention—and possible retaliation. This makes it all the more important to build a relevant, forward-looking agenda that positions BRICS within broader political debates, and strengthens cooperation and economic integration among its members, but does not contribute to rupture or increased instability in the international monetary and financial system.

References

Callen, Tim. 2007. “Purchasing Power Parity: Weights Matter.” Finance & Development Magazine 44 (1): 44-45.

Canuto, O. 2010. “Recoupling or Switchover? Developing Countries in the Global Economy.” In The Day after Tomorrow: A Handbook on the Future of Economic Policy in the Developing World, Canuto, O. & Giugale, M. (orgs.). World Bank.

Canuto, O. & Swati Ghosh. 2013. Dealing with the Challenges of Macro Financial Linkages in Emerging Markets. World Bank.

Canuto, O. 2021. Climbing a High Ladder: Development in the Global Economy. Policy Center for the New South.

Canuto, O. 2023a. “Rising Use of Local Currencies.” Policy Center for the New South, August 29, 2023.

Canuto, O. 2023b. “Growth Implications of a Fractured Trading System.” Policy Center for the New South, September 21, 2023. .

Canuto, O. 2023c. “A Tale of Two Technology Wars: Semiconductors and Clean Energy.” Policy Center for the New South, Policy Brief 41(23).

Canuto, O. 2023d. The U.S. dollar’s “exorbitant privilege” remains, Policy Center for the New South, Policy Brief 21(23).

Canuto, O. & Amshika Amar. 2024. “Emerging Markets and Developing Economies in the Global Financial Safety Net.” Policy Center for the New South, Policy Paper 01(24). .

Canuto, Otaviano & Danny Leipziger. 2012. Ascent after Decline : Regrowing Global Economies after the Great Recession. The World Bank

Canuto, O. 2024. “Whither China’s Belt and Road Initiative?” Policy Center for the New South, January 2, 2024.

Canuto, O. 2025. “The Spring of Tariff Regret.” Policy Center for the New South, May 5, 2025.

Canuto, O. & Bruno Saraiva, 2025. “Lula’s BRICS Balancing Acts in Rio.” Policy Center for the New South, July 14.

Georgieva, K. 2023. “The Price of Fragmentation.” Foreign Affairs, August 22, 2023.

G7. 1975. “Rambouillet Summit – Declaration of Rambouillet”. Ministry of Foreign Affairs of Japan, November 17, 1972.

O’Neill, Jim. 2001. “Building Better Global Economic BRICs”. Goldman Sachs Global Economics Paper 66, November 30, 2001.

O’Neill, Jim. 2021. “Will the BRICS Ever Grow Up?” Project Syndicate, September 16, 2021.

O’Neill, Jim. 2024. “The BRICS Still Don’t Matter.” Project Syndicate, October 17, 2024. .

Saraiva, B. & Otaviano Canuto. 2009. “Vulnerability, Exchange Rate and International Reserves: Whither Brazil?” Center for Macroeconomics & Development, September 21, 2009.

Wilson, D. & Roopa Purushothaman. 2003. “Dreaming with BRICs: The Path to 2050.” Goldman Sachs Global Economics Paper 99.

Zhang, P.; Canuto, O.; and Straface, F. 2025. “From Bretton Woods to Braided Path – Navigating MDB Dynamics Amid Global Shifts”. CEBRI Journal, No. 13 – January-March.

Otaviano Canuto, based in Washington, D.C, is a former vice president and a former executive director at the World Bank, a former executive director at the International Monetary Fund, and a former vice president at the Inter-American Development Bank. He is also a former deputy minister for international affairs at Brazil’s Ministry of Finance and a former professor of economics at the University of São Paulo and the University of Campinas, Brazil. Currently, he is a senior fellow at the Policy Center for the New South, a professorial lecturer of international affairs at the Elliott School of International Affairs – George Washington University, a nonresident senior fellow at Brookings Institution, and a professor affiliate at UM6P, and principal at Center for Macroeconomics and Development

Bruno Saraiva is a civil servant at the Central Bank of Brazil), having worked at the Ministry of Finance (2004-06), the World Bank (2006-07) and the Inter-American Development Bank (IDB) (2007-11). He was head of the Department of International Affairs at the Central Bank of Brazil (2011-16), alternate director for Brazil at the International Monetary Fund (IMF) (2016-24) and is currently at service at the Brazilian Ministry of Finance.

[1] A previous version of this text was published in Portuguese in CEBRI Revista Nº 13 / JAN-MAR 2025. The opinions here expressed by Bruno Saraiva are personal and do not reflect the position of the Central Bank of Brazil or the Ministry of Finance.

[2] Saudi Arabia has been invited to join BRICS+ but has not yet completed the procedures to become a member.

[3] Differentiated growth prospects and the possibility of a shift in global growth leadership was discussed in Canuto (2010).

[4] For example, see two Project Syndicate articles by Jim O’Neill (2021 and 2024) categorically stating that BRICS has not evolved to constitute an effective instance in global economic governance.

[5] Something that was already present in 2012 (Canuto and Leipziger, 2012). The pace of upward convergence of several non-advanced countries declined in the second decade of the new millennium.

[6] There is a broad consensus on the advantages of using PPP for international comparisons of the size of economies. Although GDP using PPP is more difficult to estimate, it is a more comprehensive metric because it better reflects the non-tradable goods and services sectors, and is a better measure of economic wellbeing. Furthermore, PPP exchange rates are much less volatile than market exchange rates. In its aggregations in the World Economic Outlook, the IMF uses rates estimated based on PPP. For a brief presentation of the issue, see Callen (2007).

[7] For some, the deindustrialization of the American economy would also be a symptom of this imbalance and would later help to create a political environment that questioned multilateralism and favored protectionist measures.

[8] This is despite the fact that the U.S. administration imposed higher tariffs on all trading partners, including its closest allies, with an upward differential, however, in the case of China (Canuto, 2025). A special case has been the one of Brazil: President Trump has threatened to impose a 50% tariff on the country, making references to the legal process against former President Jair Bolsonaro for a planned coup plot, as well as to measures taken by Brazil’s Supreme Court against U.S .social media platforms (Canuto & Saraiva, 2025)..

[9] In 2015, when the Chinese renminbi was approved to form part of the IMF’s Special Drawing Rights base currency basket—joining the U.S. dollar, euro, yen, and pound sterling—one of the demands was to relax restrictions between Hong Kong’s financial markets and mainland China. This was followed by a $300 billion outflow from China accounted for by Chinese individuals diversifying their financial wealth, followed by a reactivation of capital outflow controls. Without full freedom of movement, Chinese renminbi assets will not constitute a store of value for non-Chinese.

[10] IMF Managing Director Kristalina Georgieva estimated in 2023 that trade restrictions (at the time, much less relevant than those in place today) could lead to a 7% loss in global GDP (Georgieva, 2023).

[11] The BRICS have made progress on cooperation in the areas of taxation and customs, integration of payment systems, facilitation of investments in infrastructure, and cybersecurity, among other issues.

[12]The IMF has one of the largest gold stocks in the world, with 2,800 tons (90.5 million ounces), which is recorded on its balance sheet at a price of $35 per ounce. At the price of May 9, 2025 ($3,344 per ounce), the profit from the sale of 5% of the Fund’s gold stock would be able to raise around $15 billion, more than enough to finance the gap that was estimated at $8.8 billion in October 2024, to make the Poverty Reduction and Growth Fund (PRGT) self-sustaining at the new (higher) levels of demand for concessional resources from the IMF. The PRGT is the Fund’s main vehicle for providing concessional financing (currently at zero interest rates) to low-income countries (currently at zero interest rates to most LICs).

[13] In addition to the five original members, Bangladesh (2021), UAE (2021), and Egypt (2023) have already become members, and Uruguay is in the process of joining, already approved by the NDB Board of Governors. On the relationships among Multilateral Development Banks, see Zhang et al (2025).

[14] On the costs of maintaining external reserves, see Saraiva and Canuto (2009).

[15] Both issues were quite contentious in the original CRA discussions, with several of the central banks involved expressing concerns about lending resources not tied to IMF programs, as well as about assuming surveillance and possibly conditionality functions, which are now typical IMF functions.

[16] See Canuto (2023a) for a discussion of motivations and constraints for the use of local currencies in trade between BRICS countries.

[17] See Canuto (2024) for a discussion of the different phases of the BRI.